Understanding the VA Funding Fee:

For eligible veterans, active-duty service members, and surviving spouses aiming for homeownership, VA loans present a significant opportunity. These government-backed loans offer attractive interest rates, low to no down payments, and no monthly mortgage insurance, making them ideal for qualified individuals.

However, the benefits of VA loans include a caveat: the VA funding fee, a modest percentage of the loan, adds an extra cost for borrowers. This fee is crucial for understanding the overall expenses associated with obtaining a VA loan. Let’s delve into what this fee entails and its implications for homebuyers.

Understanding the VA Funding Fee

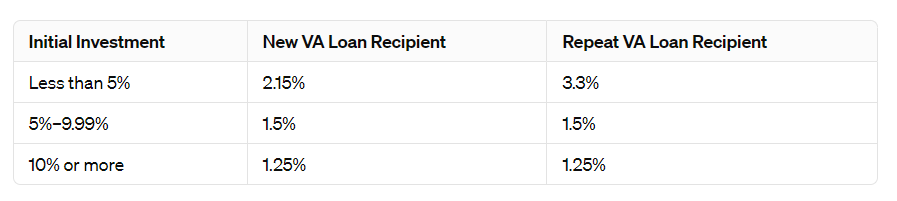

The VA funding fee, a singular payment made to the Department of Veterans Affairs, underpins the VA home loan program. Veterans contributing under 5% as a down payment face a 2.15% fee of the loan’s value on their first home purchase, with the rate increasing to 3.3% for further loans. However, increasing the down payment can reduce the fee.

Legislatively, the amount of this fee is subject to change over time.

VA Funding Fee vs. Mortgage Insurance

The VA funding fee is sometimes called VA loan PMI or mortgage insurance. It acts as the VA’s alternative to regular mortgage insurance, typically requiring just a one-time payment rather than ongoing charges.

“Funding fee,” “VA loan PMI,” and “mortgage insurance” are often used synonymously, aiming to protect the lender and the VA should a borrower default on their mortgage.

Mortgage insurance varies by loan type:

- Conventional loans necessitate monthly PMI if the down payment is below 20%.

- FHA loans require both an upfront and a monthly mortgage insurance premium for a certain duration.

- VA loans involve a singular mortgage funding fee, payable at closing or incorporated into the loan.

These terms, while specific to their respective systems, share a common goal for homebuyers.

The VA loan funding fee is levied to safeguard the lending process, ensuring the VA home loan program’s sustainability.

Rationale Behind the VA Funding Fee

VA loans are backed by the Department of Veterans Affairs, providing a safety net to lenders by insuring the loan against default. The funding fee contributes to covering these costs and additional expenses tied to the VA home loan program, securing its long-term viability.

Details on the VA Funding Fee Amount

A major advantage of VA home loans is the possibility for borrowers to secure a mortgage without any down payment. Nonetheless, opting for a higher down payment reduces the VA funding fee, directly correlating the down payment size to the fee percentage — the more you put down, the less you pay in fees.

The 2022 VA funding fee chart outlines the specific fees based on the down payment amount and whether it’s a first-time or subsequent use of the program.

In the case of a cash-out or standard mortgage refinance, individuals using the program for the first time are subject to a 2.15% funding fee, whereas those refinancing again incur a 3.3% fee. For an Interest Rate Reduction Refinance Loan, often referred to as a VA Streamline Refinance (which involves refinancing an existing VA loan into a new one), a universal funding fee of 0.5% applies to all borrowers.

Payment Methods for the VA Funding Fee

The VA funding fee is payable at closing, contributing to the overall closing costs. This fee is forwarded to the VA by your lender.

This fee represents a notable portion of closing expenses for VA loan recipients. However, it’s not mandatory to settle the entire amount upfront. Payment methods for the fee include:

- Immediate payment during closing

- Incorporation into the loan balance

- Negotiation for the seller to cover it

Incorporating the fee into your loan increases both the loan amount and monthly payments, but spreads the cost over time, avoiding a hefty upfront payment.

Sellers can also cover this fee as part of the closing costs, without the 4% concession cap that applies to other costs, offering another avenue to manage this expense.

Exemptions and Refunds for the VA Funding Fee

Not all borrowers are required to pay the VA funding fee. It’s important to verify your exemption eligibility, especially since 2020 amendments to the exemption rules now include certain Purple Heart recipients. Generally, exemptions are available to:

- Veterans receiving disability compensation due to service-related injuries.

- Veterans eligible for disability benefits who instead receive retirement or active duty pay.

- Surviving spouses who qualify for the VA home loan program.

- Active-duty service members are awarded a Purple Heart.

To determine if you qualify for a funding fee exemption, review your VA loan Certificate of Eligibility (COE), which will indicate your exemption status. If you haven’t obtained your COE yet, instructions are available on the VA’s official website.

Can You Get a Refund on the VA Funding Fee?

You might qualify for a refund of the VA funding fee if you were exempt when the fee was paid but hadn’t been recognized as such. This situation could arise if, for instance, a disability claim was pending and only approved following the completion of your home purchase.

Should your compensation eligibility date precede the closing date of your property purchase, you’re entitled to a reimbursement of the funding fee.

Conclusion: VA Loans Despite the Funding Fee

The VA home loan program stands as a highly regarded and beneficial aspect of military service. Despite the additional cost incurred by the funding fee, VA mortgages remain an excellent choice for eligible individuals, whether they are buying a new property or refinancing an existing mortgage.

Are you prepared to begin your application for a VA loan? Feel free to submit your application online or get in touch with a Home Loan Specialist now.