Remember these key points:

- An FHA loan is designed for individuals with lower credit scores or those who may not qualify for a traditional mortgage.

- This loan can be used for purchasing, constructing, or renovating a home, as well as refinancing an existing home loan.

- Borrowers opting for an FHA loan with less than a 20 percent down payment are required to pay mortgage insurance premiums in addition to their regular mortgage payments.

- FHA loans offer an opportunity for those with limited credit scores and savings for down payments to finance a home purchase. These mortgages are accessible through various lenders, including banks and independent mortgage brokers. Here is a comprehensive guide.

Understanding FHA Loans

An FHA loan is a mortgage option backed by the Federal Housing Administration (FHA), which falls under the jurisdiction of the U.S. Department of Housing and Urban Development (HUD). Although these loans are insured by the government, they are issued and funded by third-party mortgage lenders that have received FHA approval. A wide range of lenders, including large banks and various other financial institutions, provide these loans.

One of the key attractions of FHA loans is their relatively low requirements for credit scores and down payments, making them a favored choice among first-time homebuyers. With a credit score of at least 580, you could qualify for an FHA loan with just 3.5 percent down of the purchase price, or with a score of 500, you might be eligible if you can make a 10 percent down payment. The aim of these lenient underwriting criteria is to enable a broader spectrum of people to achieve homeownership.

However, there are restrictions on the types of properties that can be purchased with an FHA loan. The amount you’re eligible to borrow will depend on your creditworthiness and financial situation, adhering to the specific FHA loan limits applicable in your region. It’s also important to note that FHA loans cannot be used to acquire investment properties or vacation homes.

Ideal Candidates for FHA Loans

FHA loans are especially well-suited for individuals with lower credit scores due to past financial challenges, those who may have limited savings earmarked for a down payment, or individuals who find themselves in situations where both scenarios apply. These loans offer a viable financial solution for those looking to secure a home loan while facing credit or savings constraints.

Mechanics of FHA Loans

FHA loans function similarly to other types of mortgages, offering either fixed or adjustable rates and terms typically set at 15 or 30 years.

When securing an FHA loan, borrowers will encounter closing costs, including appraisal fees and origination charges. Notably, the FHA permits sellers, builders, or lenders to contribute up to 6 percent towards these expenses.

To safeguard against defaults — situations where a borrower fails to continue loan repayments — the FHA mandates that borrowers making less than a 20 percent down payment must pay Mortgage Insurance Premiums (MIP). These payments are directed into the Mutual Mortgage Insurance Fund (MMIF), which is designed to handle claims for losses. Although it’s the borrower who pays these premiums, the purpose of FHA mortgage insurance is to offer protection to the lender.

Eligibility Criteria for FHA Loans

Below is a summary of what you need to qualify for an FHA loan:

- Credit Score Requirements: A minimum score of 580 qualifies you for a 3.5 percent down payment, while a score between 500 and 579 requires at least a 10 percent down payment.

- Down Payment Needs: A down payment of at least 3.5 percent is needed if your credit score is 580 or above. For scores between 500 and 579, the down payment requirement is at least 10 percent.

- Debt-to-Income Ratio: Generally, your DTI ratio should not exceed 43 percent, though there may be flexibility up to 50 percent in certain scenarios.

- Property Use: The loan must be for your primary residence, and the property can have between one and four units.

- Loan Limits: The standard loan limit is $498,257 for a single-unit property in most areas, with higher limits in more expensive areas, Alaska, Hawaii, and for multi-unit properties.

- Mortgage Insurance: Includes an upfront premium of 1.75 percent of the loan amount, paid at closing, and annual premiums ranging from 0.15 percent to 0.75 percent, depending on various factors, typically paid monthly.

Varieties of FHA Loans

FHA loans come in several forms, including:

- Standard Home Mortgage (203(b) Loan): This primary FHA loan program offers fixed and adjustable rate options with 15- or 30-year terms.

- Rehabilitation Mortgage (203(k) Loan): The 203(k) loan finances both the purchase and renovation of a home, available in Standard and Limited versions based on renovation costs and types.

- Disaster Victims Mortgage (203(h) Loan): For those who have lost their homes due to a significant disaster, this loan offers a path to rebuild or buy a new home without a down payment requirement.

- Home Equity Conversion Mortgage (HECM): An FHA-insured reverse mortgage that allows individuals over 62 to convert their home equity into tax-free income.

- Energy Efficient Mortgage (EEM): Aimed at financing the purchase of an energy-efficient home or upgrading a home for better energy efficiency.

- Graduated Payment Mortgage (245(a) Loan): A less common mortgage type with initially low payments that gradually increase, designed for individuals expecting future income growth.

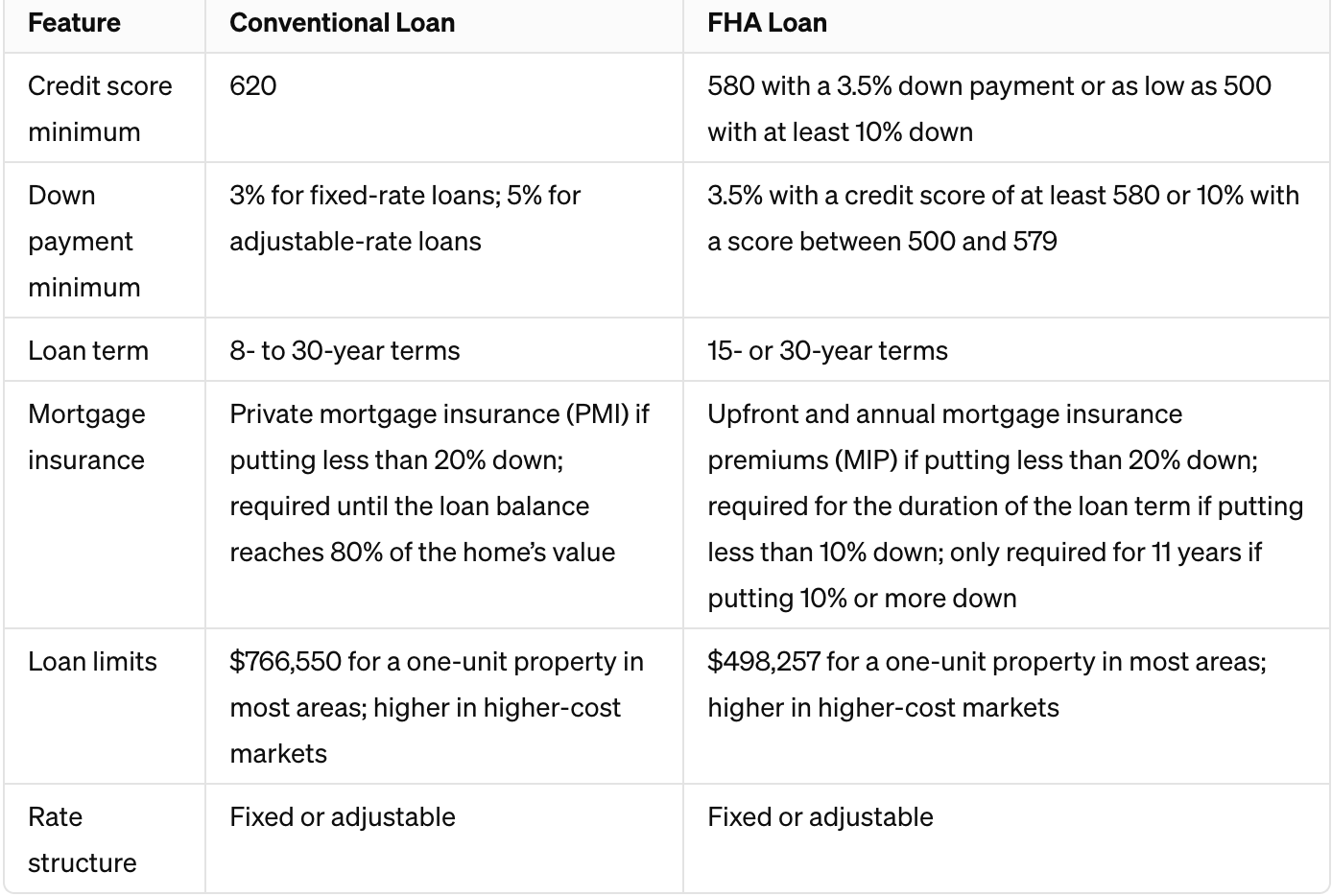

Comparing FHA Loans with Conventional Mortgages

Conventional mortgages rank as the most commonly chosen type of home loan. In contrast to FHA loans, conventional loans do not carry government insurance. Below is a direct comparison between the two:

Advantages and Disadvantages of FHA Mortgages

Advantages:

- Accessible Credit Score Requirements: FHA loans offer a path to homeownership for those with credit scores starting at 580 or even as low as 500, depending on the down payment amount.

- Minimal Down Payment: For those with a credit score of 580 or higher, FHA loans allow for down payments as low as 3.5 percent.

- Quicker Path to Homeownership: The more lenient qualifications associated with FHA loans can enable buyers to purchase a home and begin accumulating equity earlier than they might otherwise.

Disadvantages:

- Unavoidable Mortgage Insurance: All FHA loan holders are required to pay an upfront mortgage insurance premium (MIP), and those who make a down payment of less than 10 percent must continue paying annual MIP for either the life of the loan or until refinancing or selling. A down payment of 10 percent or more reduces this obligation to 11 years.

- Property and Use Limitations: There are caps on how much you can borrow with an FHA loan, which vary by location. Additionally, FHA loans mandate that the property be your primary residence, excluding second homes or investment properties.

- Potential for Higher Overall Costs: While FHA loans may offer lower interest rates compared to conventional loans, their annual percentage rates (APRs), which include all borrowing costs such as fees and points, could be higher.

FHA Loan Frequently Asked Questions

Is an FHA Loan Suitable for You?

Choosing an FHA loan could be a smart move if you’re dealing with a lower credit score or have limited funds for a down payment. This loan type is particularly appealing because it accommodates financial situations that might not meet the criteria for conventional loans. However, FHA loans do come with higher costs due to mortgage insurance premiums. If your credit score is 620 or above, you might be eligible for a conventional mortgage with potentially lower costs over time, especially since you can remove private mortgage insurance (PMI) once you achieve 20 percent equity in your home.

How to Apply for an FHA Loan?

To begin the application process for an FHA loan, first verify that you qualify based on the program’s credit score and debt-to-income ratio requirements. Utilize an affordability calculator to gauge what you can afford by considering your income, expenses, and the amount you can put towards a down payment. Then, research and compare lenders to apply for the best loan option. Be prepared to provide documentation such as the last two years of tax returns, recent pay stubs, valid identification, and complete asset statements from your bank accounts and any investment accounts.

Comparing FHA Loans to Other Types of Loans

FHA loans are known for their lenient credit score requirements and mandate for mortgage insurance on down payments less than 20 percent, similar to conventional loans. Unlike VA loans and USDA loans—which are exclusively available to military personnel, veterans, their spouses, and low- to moderate-income buyers in designated rural areas respectively—FHA loans are accessible to a broader range of applicants who meet the qualifications.

Eliminating FHA Mortgage Insurance

Mortgage insurance is mandatory for all FHA loans. If your initial down payment is 10 percent or more, you can remove the FHA mortgage insurance after 11 years. For those who make a down payment of less than 10 percent, mortgage insurance payments continue until the loan is fully repaid, the property is sold, or you refinance into a conventional mortgage.