Maximizing Your VA Loan Benefits:

The VA loan program offers veterans, active-duty members, reservists, National Guard members, and eligible spouses mortgage options with no down payment or PMI required.

Many have benefited from this Department of Veterans Affairs (VA) housing perk. However, if you’re struggling with VA loan payments, consider a VA Interest Rate Reduction Refinance Loan (IRRRL) to lower your interest rate.

Here’s an overview of the VA IRRRL, its advantages and disadvantages, and how it fits your financial needs.

Understanding VA IRRRL

A VA IRRRL, also called a VA Streamline, is a simple and quick way to refinance your loan. This process lets you change from a changing-rate mortgage to a steady-rate one, lower your monthly interest, or adjust how long you have to pay back the loan. You need to already have a VA loan to use a VA Streamline.

If you want to turn the value of your home into cash, you’ll need to go through a complete VA cash-out refinance.

How VA Streamline Refinance Works

“Streamline” means making the refinance process easier and cheaper. Normally, when you refinance, it’s like buying your home all over again with all the steps and fees. But with a streamline, you often don’t need a new home check (appraisal) and the paperwork is simpler. Your bank might check your credit score and job, but the VA isn’t as strict. If you’re keeping up with your current mortgage, you’re likely good for a streamline loan.

You’ll still need to do a title search and buy title insurance for your bank. This quick process can roll the closing costs into your new loan.

The VA says you can only use a VA Streamline if it clearly saves you money right away, like getting a lower monthly payment or interest rate. You can’t use it just to change lenders or for reasons that don’t improve your money situation.

Advantages and Disadvantages of VA IRRRL

The VA IRRRL program offers a range of benefits designed to make refinancing more appealing and accessible to eligible veterans and service members. However, like any financial decision, it comes with its considerations. Here’s a breakdown of the pros and cons:

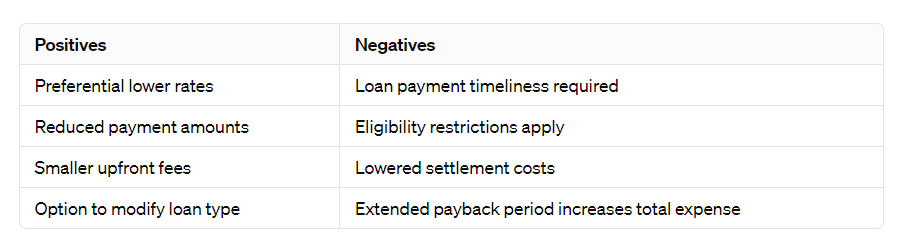

Pros of VA IRRRL Streamline Refinance

Benefits of the VA Streamline Program:

- Reduced Interest Rates: Veterans often refinance their loans to benefit from lower interest rates with the VA Streamline, particularly aiming for rates lower than their original loans unless they’re moving from an ARM.

- Decreased Monthly Payments: Utilizing the VA Streamline could lead to reduced monthly payments, either through securing a lower interest rate or extending the loan term, providing more time to pay the mortgage.

- Minimal Funding Fee: Unlike regular VA loans that charge a funding fee between 1.25% and 3.3%, the VA Streamline requires only a 0.5% fee, making it more affordable upfront.

- Change in Mortgage Type: This refinancing option allows for the transition from an adjustable to a fixed-rate mortgage, offering stability against rate fluctuations.

Cons of VA IRRRL Streamline Refinance

Limitations and Costs:

- Requirement for Current Payments: Eligibility requires that you are up-to-date on your mortgage, with no payment more than 30 days late in the past 6 to 12 months.

- Property Restrictions: The VA Streamline is strictly for refinancing the loan on your current property under a VA loan, not for transferring the loan to a new property.

- Eligibility Criteria: To apply, you need an existing VA loan and must demonstrate that the refinance will benefit you financially, which might be challenging for some.

- Associated Costs: Despite potentially lower closing costs, borrowers must still consider the funding fee and the option to roll these expenses into the new loan, affecting the total loan cost.

- Loan Duration: Refinancing doesn’t necessarily mean extending your mortgage term; however, doing so can lead to paying more over time, which might not suit everyone.

- Seasoning Requirement: You must have made six consecutive monthly payments on your existing loan and wait at least 212 days from the first mortgage payment to the Streamline closing.

A Quick Overview of Pros and Cons of VA IRRRL

Eligibility for VA IRRRL Refinance

Ready to refine your mortgage terms with ease? Dive into the clear-cut eligibility criteria for the VA IRRRL and see if you can start saving on your home loan now.

You Need a VA Loan Already

To use IRRRL, you must already have a home loan from the VA. It’s for changing your current loan’s details, not for switching from a different kind of loan.

You Lived in the Home Before

To get IRRRL, you need to have lived in the house that you got the VA loan for, just like the VA says you should.

It Should Save You Money

Refinancing with IRRRL is all about making your loan cheaper or better for you, like getting a smaller interest rate or lower house payments every month. It should help you save money compared to what you’re paying now.

Who Should Consider a VA IRRRL Loan?

The VA IRRRL is a strategic option for specific individuals within the veteran and military community. It is particularly suited for those seeking to lower their monthly mortgage payments, which can be achieved through securing a lower interest rate or extending the loan term. This can significantly relieve families looking to enhance their monthly financial flexibility.

Furthermore, the IRRRL is an excellent choice for borrowers currently navigating the unpredictability of an adjustable-rate mortgage (ARM). Switching from an ARM to a fixed-rate mortgage through the IRRRL process can offer a stable, predictable payment schedule, protecting against future interest rate increases and facilitating better financial planning.

Eligibility to apply for a VA IRRRL is not just about meeting formal criteria; it’s also about demonstrating a tangible net benefit from the refinance. This means that potential applicants should carefully consider how the refinancing will affect their overall financial health, including both immediate benefits and long-term financial commitments.

Individuals who can prove that refinancing will provide them with a clear economic advantage, such as reducing overall loan costs or improving loan terms, are the ideal candidates for a VA IRRRL loan.

Applying for a VA IRRRL Loan

Embarking on the journey to secure a VA Interest Rate Reduction Refinance Loan (IRRRL) is streamlined into a series of steps to ensure a smooth application process. Here’s a guide to navigating the application:

- Confirm Your Eligibility: The first step is to verify that you meet the criteria for a VA IRRRL. This includes having an existing VA loan and ensuring the refinanced loan offers a tangible financial benefit.

- Gather Necessary Documentation: Prepare the required documents, which typically include your current mortgage details, proof of eligibility for the VA loan, and any other financial documents your lender may request to assess your situation.

- Consult with a Home Loan Expert: Contact a mortgage advisor or home loan expert specializing in VA loans. They can provide personalized advice, help you understand the nuances of the IRRRL program, and guide you through the application process.

Required Documentation and Expert Advice:

The documentation required typically includes but is not limited to, a valid Certificate of Eligibility (COE), loan summary sheet, proof of residence, and any relevant financial statements. Additionally, consulting with a home loan expert can provide:

- Insights into optimizing your application.

- Understanding current rates.

- Ensuring that your refinance aligns with your financial goals.

VA IRRRL FAQs

Can I get money back from a VA IRRRL refinance?

Generally, the VA IRRRL is not designed for cash-back refinancing. However, exceptions exist, such as being reimbursed for up to $6,000 in energy-efficient home improvements completed within 90 days before closing.

How much does the VA IRRRL cost?

The costs associated with a VA IRRRL are typically lower than those of traditional refinancing options. Expect closing costs to be between 2% and 5% of the loan amount, including a 0.5% funding fee that can be rolled into the loan balance. Some lenders may offer to cover costs through higher interest rates or other means.

Can I buy discount points to lower my interest rate?

Yes, the VA allows borrowers to purchase up to two discount points to reduce their interest rate, potentially leading to significant savings over the life of the loan.

Can I use the VA Streamline Refinance for an investment property?

The VA IRRRL is primarily intended for properties that are or were the borrower’s primary residence. If the property was once your primary residence but is now an investment property, you may still be eligible to refinance with an IRRRL.

Conclusion

The VA IRRRL is a practical choice for veterans and their families aiming to reduce their mortgage payments or improve loan terms with ease. By evaluating your finances and consulting with a loan specialist, you can navigate this process smoothly. Reach out to a VA loan provider or check the VA website to begin your journey toward a more stable financial future.