Debt-To-Income (DTI) Ratio For VA Loans

When seeking a home loan, the debt-to-income ratio (DTI) plays a crucial role in determining your eligibility. This is also true for a VA loan, which is a government-backed home loan available to active-duty military members, veterans, or their surviving spouses.

Understanding your DTI beforehand can be beneficial. This metric informs the lender about your capacity to manage new debt given your existing financial obligations relative to your income. A high DTI might lead lenders to view you as a higher risk, potentially resulting in a rejection of your application. Here’s an in-depth exploration of the debt-to-income ratio requirements for VA loans and strategies for enhancing your DTI if it falls short of the required standards.

What Does Debt-To-Income (DTI) Mean?

Debt-to-income ratio, or DTI, is a measure that compares your monthly debt obligations to your gross monthly income. Essentially, it calculates the portion of your pre-tax monthly income that goes towards paying off debts like car loans, rent, credit card bills, and mortgages.

When you apply for a standard mortgage or an unconventional loan like a VA loan, lenders assess your DTI to gauge whether you can manage the new debt you intend to acquire. Generally, applicants with lower DTIs are seen in a more positive light as it suggests they pose less of a risk compared to those with higher debt levels who may struggle to meet their monthly payments under financial stress.

To figure out your DTI, sum up all your minimum monthly debt payments (including payments for autos, mortgages, credit cards, etc.) and divide this total by your gross monthly income.

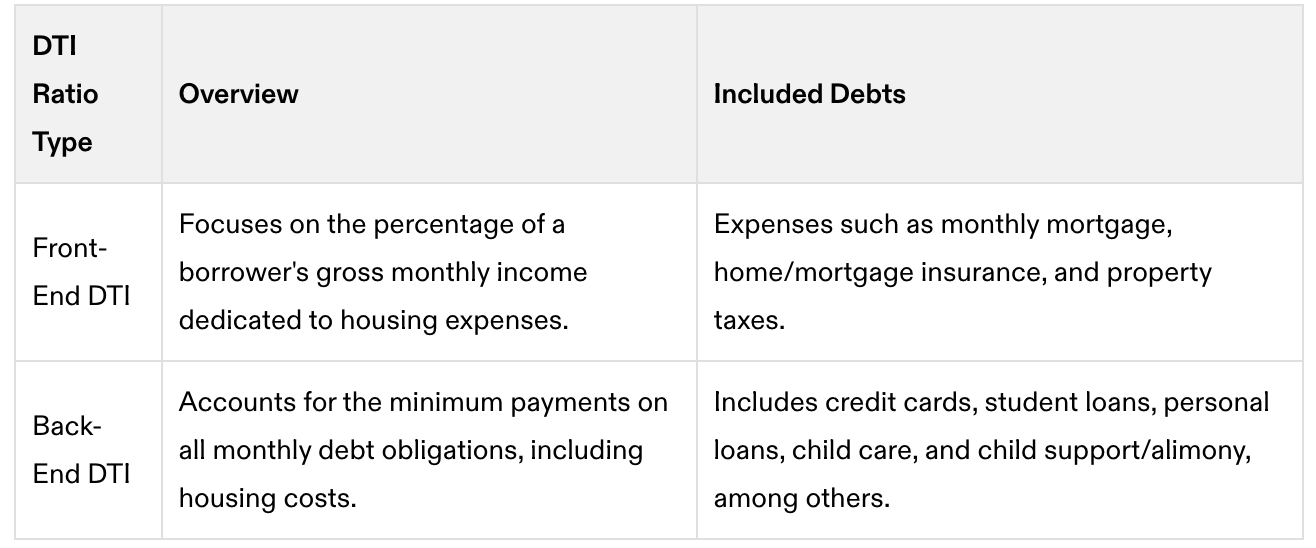

Front-End DTI Versus Back-End DTI

In the process of mortgage underwriting, lenders evaluate both your front-end and back-end DTI. The front-end DTI focuses solely on your housing-related expenses, which encompasses mortgage payments, homeowners’ insurance, property taxes, and any homeowners association fees applicable to your area.

On the other hand, the back-end DTI takes into account all your minimum monthly debt obligations. This includes not just housing costs but also other monthly liabilities such as student loans, credit cards, and personal loans. In essence, this calculation considers all your existing debt commitments.

What’s the Highest DTI Allowed for a VA Loan? The optimal debt-to-income (DTI) ratio for securing a VA loan is typically 41%. However, it’s crucial to understand that the Department of Veterans Affairs doesn’t enforce a strict maximum DTI limit. Instead, it offers guidelines for lenders who then decide on their own caps, considering factors like the applicant’s creditworthiness and other financial details.

This flexibility means that obtaining a VA loan with a DTI higher than 41% is indeed possible. Therefore, it’s advisable to inquire directly with your lender about their specific DTI requirements to gauge your loan eligibility chances.

How to Calculate Your DTI for a VA Loan Knowing the significance of DTI in the VA loan approval process, here’s a step-by-step guide to calculating yours:

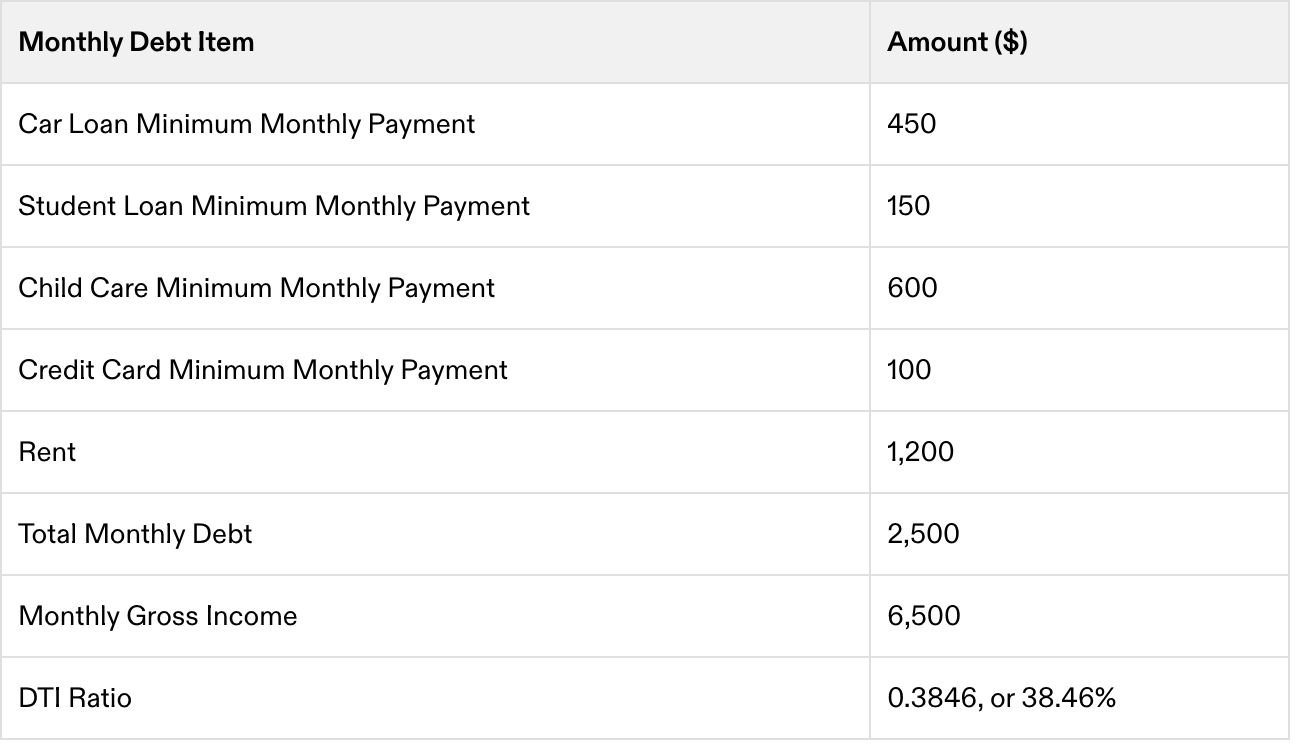

Sum Up Your Monthly Debt Payments Start by tallying the minimum amounts due for all your monthly debts. This calculation should include the lowest payment you’re obligated to make each month, regardless of any temporary increases in your account balances. Common types of monthly debts include:

- Rent or mortgage

- Homeowners association dues

- Auto loans

- Educational loans

- Personal loans

- Child support or alimony payments Note that daily living expenses, such as food and transportation, are not part of this calculation.

Divide Total Monthly Debt by Gross Monthly Income Then, figure out your gross monthly income, which is the total amount of money you earn before taxes each month. If you’re applying for the loan alone, only your income counts. If you’re applying with another person, like a spouse, you can include their income too. After determining your gross monthly income, divide your total monthly debt obligations by this amount.

Convert the Result to a Percentage The division will yield a decimal number. Convert this decimal into a percentage by multiplying it by 100. This final percentage is your DTI ratio.

Based on the guidelines for VA loans, the borrower described in the previous example would be eligible for a VA loan, given that their DTI is below the 41% threshold.

What to Do If Your DTI Exceeds 41%?

Having a DTI ratio above 41% doesn’t necessarily close the door on qualifying for a VA home loan, but it might lead to more detailed financial evaluations.

Options for Qualifying with a Higher DTI

- Additional Residual Income: One pathway to loan qualification despite a higher DTI involves demonstrating sufficient residual income. VA loans mandate a certain level of residual income, which is the cash remaining after settling all monthly debts. The exact requirement varies by factors such as loan size, family size, and geographical location. Should your DTI surpass 41%, you’ll need to exceed the standard residual income threshold by at least 20%. For instance, if the standard requirement is $1,800 for those under the 41% DTI cap, you’d need $2,160 if your DTI is higher.

- Inclusion of Tax-Free Income: Sometimes, a higher DTI could be due to tax-free income sources, such as military allowances, workers’ compensation, child support, or disability benefits. These are not factored into the DTI calculation. In such cases, lenders might consider this income during the loan evaluation process.

- Adjusting Home Budget: Your loan size directly influences your DTI. Opting for a smaller loan might make it easier to qualify even with a higher DTI. It’s essential to discuss with your lender what loan sizes and corresponding DTI levels are acceptable.

Strategies to Lower Your DTI for VA Mortgage Loan

Lowering a high DTI is achievable with several strategies:

- Eliminate Monthly Payments: Clearing small debts can effectively reduce your DTI. Whether it’s a credit card balance or a student loan, eliminating these debts can improve your ratio.

- Boost Your Income: Increasing your income through freelancing, side gigs, seasonal jobs, or securing a raise can help. Ensure any additional income meets the lender’s criteria for consistency and stability. Military personnel may need approval for secondary employment.

- Include Another Borrower: Adding another borrower, like a spouse, to your application might aid in meeting the loan qualifications. However, this can either lower or raise your DTI depending on the co-borrower’s financial situation.

- Delay Your Application: If necessary, postponing your loan application gives you time to organize your finances, pay down debt, and enhance your income.

Final Thoughts

Your DTI ratio is a crucial metric for lenders, offering a snapshot of your financial health by comparing your debt to your income. A lower DTI is a positive indicator for VA lenders, signifying a lower risk. However, if your DTI is on the higher side, know that there are avenues to qualify for a VA loan and methods to reduce your DTI before seeking a mortgage. Check your eligibility for a VA home loan or explore other mortgage options by seeking pre-approval from lenders like Elevation Mortgage.