PMI vs. VA Funding Fee Explained

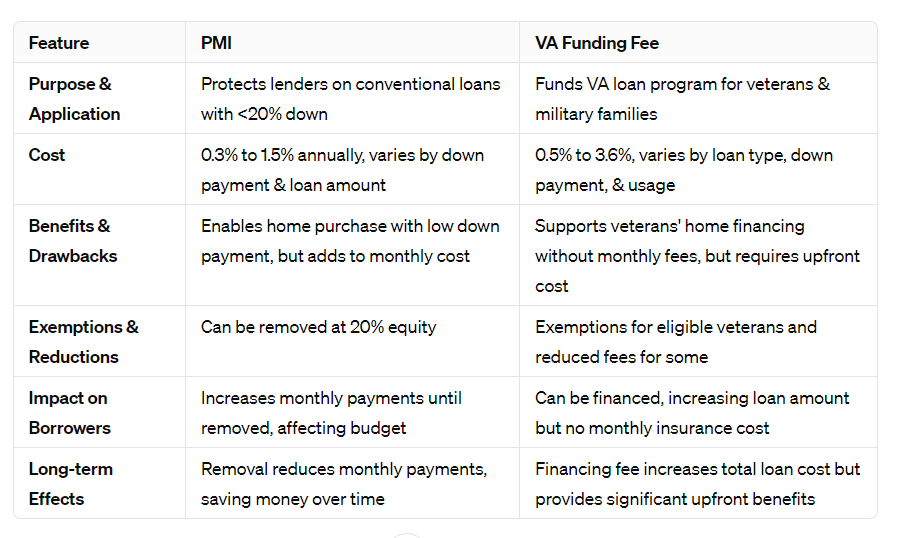

When navigating the world of home buying, two terms frequently emerge: Private Mortgage Insurance (PMI) and the VA Funding Fee. PMI is a type of insurance that conventional loan borrowers may need to pay if their down payment is less than 20%, designed to protect the lender from the risk of default.

On the other hand, the VA Funding Fee is a one-time fee paid by veterans, service members, and select military spouses who take out VA loans. This fee helps fund the VA home loan program, ensuring its continued availability for future generations. Both PMI and the VA Funding Fee have significant implications for borrowers and lenders, influencing loan eligibility, costs, and overall affordability of home financing.

What is PMI?

Private Mortgage Insurance (PMI) serves as a safeguard for lenders against the possibility of a borrower defaulting on a mortgage. Required for conventional loans with less than a 20% down payment, PMI helps broaden homeownership opportunities by enabling individuals to purchase homes without needing to save for a large down payment.

PMI costs vary, typically ranging from 0.3% to 1.5% of the original loan amount annually, and can be removed once the borrower has enough equity in their home. Avoiding PMI is possible by making a 20% down payment, obtaining a lender-paid mortgage insurance (LPMI) arrangement, or choosing loan programs that don’t require PMI.

What is the VA Funding Fee?

The VA Funding Fee is a mandatory fee for most borrowers of VA home loans, designed to fund the VA loan program and sustain it for future veterans and military members. Unlike PMI, which is an insurance protecting the lender, the VA Funding Fee supports the VA’s loan guarantee, which protects the lender without monthly premiums.

The amount of the fee varies depending on the type of loan, the size of the down payment, whether the borrower is using the VA loan benefit for the first time, and other factors. Exemptions from the VA Funding Fee are available for eligible veterans, such as those receiving VA disability compensation and select others. This fee can be financed into the loan amount or paid upfront at closing, offering flexibility to the borrower.

Comparing PMI and VA Funding Fee

Unlock the secrets to smarter home buying! Dive into the world of PMI and VA Funding Fees where understanding the difference could save you thousands. Are you ready to make an informed decision?

Final Words

Navigating the financial landscape of home buying reveals critical choices between conventional loans with PMI and VA loans with their unique funding fee. Each option offers distinct advantages and considerations, impacting immediate financial outlays and long-term mortgage expenses. For eligible veterans, the VA loan’s funding fee facilitates access to beneficial loan terms, whereas conventional loan borrowers evaluate PMI’s impact on their monthly payments and overall home affordability. Making an informed decision requires understanding these costs, their exemptions, and their long-term implications on homeownership finances.