A Comparative Analysis of VA and Conventional Loans

Navigating the vast world of home financing options can be a daunting task for prospective homebuyers. Understanding the different types of loans available is crucial in making an informed decision that aligns with one’s financial goals and circumstances. This comparison focuses on two major types of mortgage loans: Veterans Affairs (VA) loans and conventional loans.

Each loan type offers distinct advantages and eligibility criteria, catering to different borrower needs. By examining these options side by side, borrowers can gain insights into which loan might offer them the best terms, interest rates, and benefits, thus making a pivotal step towards homeownership both informed and strategic.

What Are VA and Conventional Loans?

VA Loans

VA loans are a powerful benefit of military service, offering significant advantages to eligible veterans, active-duty service members, and certain surviving spouses. These loans are backed by the U.S. Department of Veterans Affairs, enabling lenders to offer them with favorable terms.

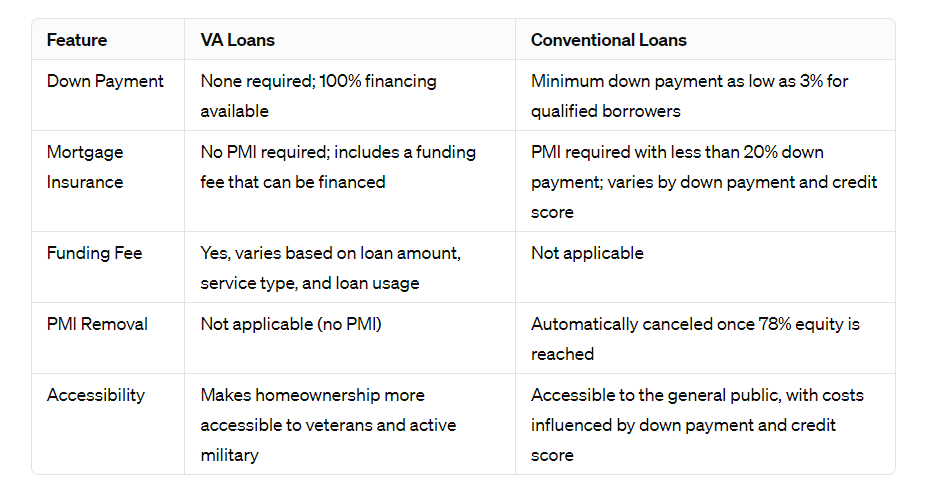

A hallmark feature of VA loans is the absence of a down payment requirement, making homeownership accessible without the need for substantial savings upfront. Additionally, borrowers are not required to pay for private mortgage insurance (PMI), a common expense for other loan types when the down payment is less than 20%. This can result in considerable monthly savings, further reducing the financial barriers to purchasing a home.

Conventional Loans

Conventional loans, on the other hand, are the most popular mortgage option in the housing market. Unlike VA loans, they are not backed by any government agency, which means they are offered through private lenders. This type of loan tends to have stricter credit scores and down payment requirements but provides a great deal of flexibility in terms of property types and uses.

Conventional loans can be used to purchase primary residences, second homes, or investment properties. While they generally require a down payment, advancements in mortgage products have introduced options with down payments as low as 3% for qualified borrowers.

Despite the need for PMI with down payments of less than 20%, conventional loans remain a preferred choice for many, especially those without military service or who are investing in additional properties.

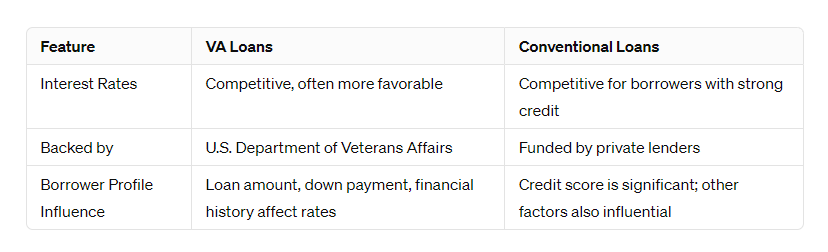

Interest Rates Comparison

Unlock the secrets to maximizing your savings! Dive into our Interest Rates Comparison table and discover the best rates to grow your wealth effortlessly.

Credit Score Requirements

Flexibility of VA Loans

One of the most borrower-friendly aspects of VA loans is the lack of a set minimum credit score by the Department of Veterans Affairs. This flexibility allows lenders to evaluate borrowers on a case-by-case basis, potentially approving loans for individuals with lower credit scores. However, it’s common for lenders to establish their credit score minimums to mitigate risk, often requiring a score of 640 or higher. This flexibility underscores the VA loan program’s commitment to assisting veterans and active military members in achieving homeownership.

Conventional Loans’ Credit Standards

In contrast, conventional loans typically adhere to stricter credit score requirements, with most lenders requiring a minimum score of 620. This benchmark is set by mortgage giants Fannie Mae and Freddie Mac and serves as a baseline for borrower eligibility. Higher credit scores not only increase the likelihood of loan approval but also potentially secure lower interest rates for the borrower. As such, for those considering conventional financing, focusing on credit health is crucial.

Impact on Borrower Options

The differing credit score requirements between VA and conventional loans highlight the importance of understanding one’s credit profile when exploring mortgage options. For eligible veterans and service members, VA loans offer a path to homeownership even with a less-than-perfect credit score. Meanwhile, potential borrowers with strong credit scores might find conventional loans to be a viable option, especially if they are looking for flexibility in terms of property type and use. Navigating these requirements effectively can help borrowers secure favorable loan terms, aligning with their financial goals and homeownership aspirations.

Down Payment and Mortgage Insurance

Navigate the path to homeownership with ease! Explore our Down Payment and Mortgage Insurance comparison table for a clear roadmap to securing your dream home

Property Restrictions and Loan Usage

VA Loans

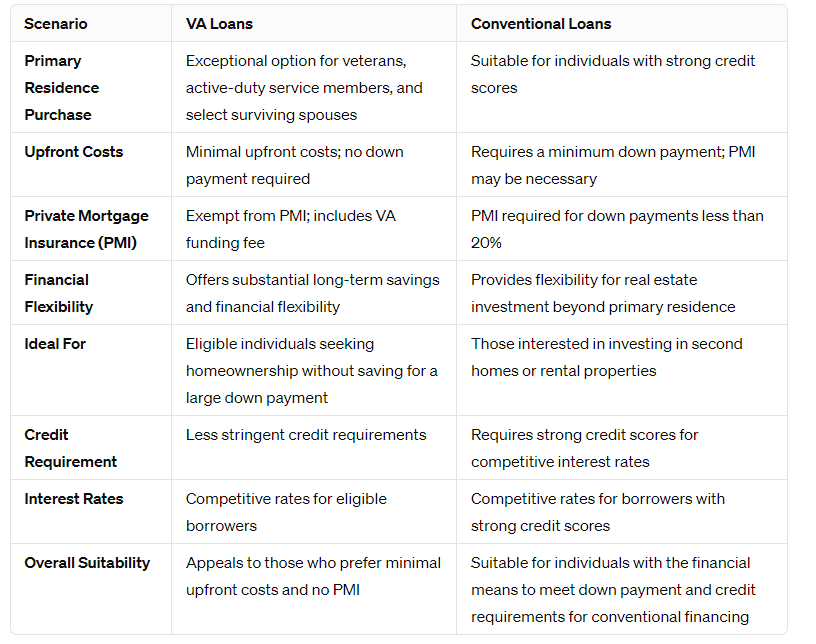

VA loans are specifically designed to help veterans, active-duty service members, and eligible surviving spouses become homeowners. As such, they come with certain restrictions, the most notable being that the purchased property must be the borrower’s primary residence.

This means that VA loans cannot be used to buy second homes, investment properties, or vacation homes. The VA’s emphasis on primary residences ensures that the benefits of the loan program are directed toward helping veterans and service members secure stable and affordable housing.

Conventional Loans

Conversely, conventional loans offer greater flexibility in terms of how the borrowed funds can be used. Borrowers can use conventional loans to purchase primary residences, second homes, or investment properties. This flexibility makes conventional loans a popular choice for a wider range of buyers, including those looking to invest in real estate or purchase vacation homes. However, it’s worth noting that the terms and requirements for conventional loans can vary more significantly than those for VA loans, especially regarding down payments and credit scores for second homes or investment properties.

When Each Loan Type Makes Sense

Conclusion

Choosing between a VA loan and a conventional loan hinges on understanding their unique benefits and assessing which aligns best with your financial situation and homeownership goals. VA loans offer significant advantages for eligible military members, facilitating homeownership with minimal upfront costs and no PMI. Conversely, conventional loans appeal to a broader audience, especially those with strong credit scores or investment ambitions, despite requiring a down payment and PMI for lower down payments. Careful consideration of each option’s features against your financial backdrop and objectives will guide you toward the most suitable path to securing your home.