A Comprehensive Loan Limits Comparison:

VA home loans are a cornerstone of financial support for veterans and active military members, offering a path to homeownership under favorable terms. These loans, guaranteed by the U.S. Department of Veterans Affairs, facilitate purchasing, constructing, or refinancing a home for personal occupancy. VA loans stand out for their unique benefits, including no minimum payment or private mortgage insurance (PMI) requirement, lower interest rates, and flexible credit guidelines, making homeownership more accessible to those who have served our country.

A significant milestone in the evolution of VA home loans came with the Blue Water Navy Vietnam Veterans Act of 2019. This landmark legislation expanded the benefits for Vietnam War veterans exposed to Agent Orange, and notably, it also made critical adjustments to VA home loan limits.

Before this Act, VA loans were capped at specific amounts, restricting the buying power of veterans in many parts of the country. The Act’s passage effectively eliminated these loan limits for borrowers with full entitlement, thus broadening access to housing in high-cost areas and enhancing the purchasing power of eligible service members, veterans, and survivors.

Understanding VA Home Loan Limits

Before 2020, VA home loan limits were pivotal in determining the maximum amount the VA would guarantee for a home loan. These limits were aligned with the conforming loan limits set by the Federal Housing Finance Agency (FHFA), restricting the loan amount a veteran could borrow without needing to make a down payment. These caps were designed to reflect the median home price in different areas, aiming to balance the program’s benefits with the realities of the housing market. The full entitlement is at the heart of understanding VA home loan limits post-2019.

Veterans and active military members with full entitlement no longer face these borrowing caps. Full entitlement means that a borrower has yet to use their VA loan benefit or has fully restored it after paying off a previous VA loan. This change significantly impacts eligible borrowers, allowing them to secure financing above the conforming loan limits without a down payment, subject to their lender’s credit requirements. This shift reflects a broader commitment to supporting veterans in their post-service life, recognizing the need to facilitate more significant financial opportunities for those who have served.

By removing the loan limits for those with full entitlement, the VA has underscored its dedication to veterans’ welfare, acknowledging the diverse needs and financial realities faced by service members across the country. This adjustment ensures that VA loans remain a potent tool for veterans aiming to secure a piece of the American dream: homeownership.

2024 VA Loan Limits Overview

The landscape of VA loan limits has undergone significant transformations, particularly following the Blue Water Navy Vietnam Veterans Act of 2019. For 2024, the standard loan limit for VA loans aligns with the conforming loan limits set by the Federal Housing Finance Agency (FHFA). In most U.S. counties, this limit is $766,550, offering a substantial baseline for veterans and active military members seeking to purchase a home without a down payment. This standardization provides clarity and consistency for applicants nationwide, ensuring that VA loan benefits are accessible to a broad audience.

However, recognizing the diversity of the U.S. real estate market and the varying cost of living across different regions, the VA loan program adjusts its limits for high-cost counties. In these areas, the loan limits are elevated to accommodate the higher price of real estate, thereby extending the purchasing power of veterans and active military members.

For instance, counties such as San Francisco, CA, and Honolulu, HI, have higher limits, reflecting the premium on housing in these locales. Specific examples include counties like Pitkin, CO, and Nantucket, MA, where the loan limits can reach up to $1,149,825, providing significant leverage to borrowers in these high-cost areas.

Eligibility and Entitlement

Eligibility for full entitlement under the VA loan program is a cornerstone for accessing these increased borrowing capacities. The full entitlement is available to those who have never utilized their VA home loan benefit and individuals who have repaid a previous VA loan in full and sold the property or who have repaid the VA in full following a foreclosure or short sale. This broad criterion aims to ensure that veterans and active military members have maximal opportunity to benefit from the VA loan program, recognizing their service and sacrifice.

The impact of full entitlement on loan limits is profound. For eligible borrowers, it means the possibility of securing a home loan that exceeds the standard conforming loan limits without needing a down payment. This aspect of the VA loan program is especially beneficial in high-cost areas, where the median home price outpaces the standard loan limits. By allowing veterans and active military members to purchase homes without a down payment, the VA loan program stands out as a uniquely supportive mechanism in the pursuit of homeownership, acknowledging the diverse financial and geographic realities faced by those who have served.

In essence, the VA loan limits for 2024, coupled with the criteria for full entitlement, underscore a commitment to providing flexible and substantial support to veterans and active military members in their homeownership journey. This framework ensures that the benefits of the VA loan program are tailored to meet the needs of its beneficiaries, offering a pathway to homeownership that is both accessible and responsive to the market dynamics across the United States.

Special Considerations for VA Loans

For veterans and active military members without full entitlement, VA loan limits still play a crucial role in determining how much they can borrow. This distinction is particularly important for those who have previously utilized their VA loan benefits and have not fully restored their entitlement.

In such cases, the VA loan limits are defined by the conforming loan limits set by the Federal Housing Finance Agency (FHFA) for the specific county where the property is located. Borrowers might encounter these loan limits if they have an active VA loan on another property, have not repaid a previous VA loan in full, or have experienced a foreclosure or short sale without fully repaying the VA.

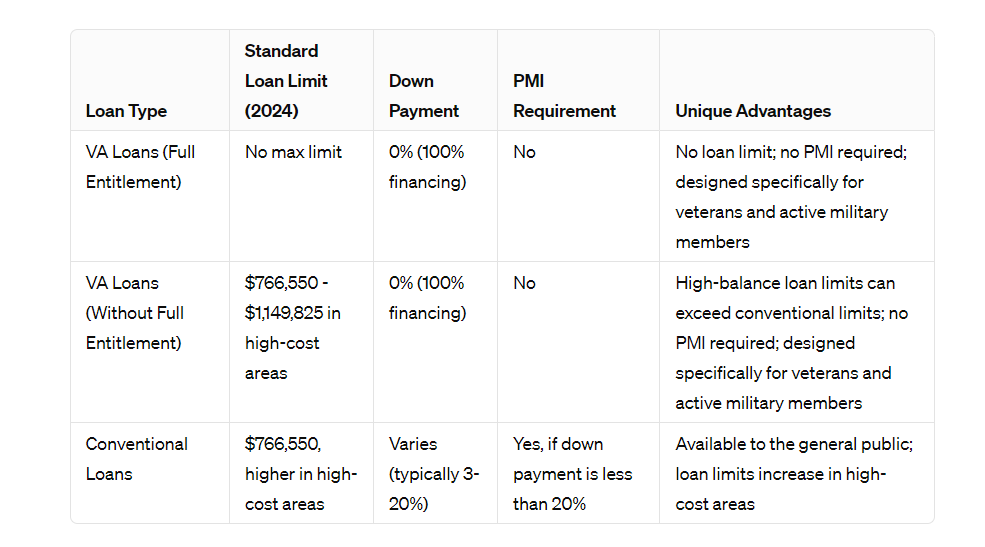

Comparing VA Loan Limits with Other Loan Types

When comparing VA loan limits with those for conventional loans in 2024, it’s evident that VA loans offer distinct advantages.

Conclusion

With its variable limits tailored to entitlement levels and geographic locations, the VA loan program showcases a solid commitment to enabling homeownership for veterans and active military members. Its flexible structure caters to high-cost areas and accommodates individuals without full entitlement, demonstrating a thoughtful approach to meet the varied needs of its users. By removing loan limits for fully entitled beneficiaries and offering advantages over traditional loan options, the VA loan program emerges as a top-tier financing choice for home purchases. It encourages veterans and active military personnel to utilize its unique benefits, such as 100% financing and no requirement for PMI, making it an effective avenue toward homeownership. This has a profound positive impact on their financial health and allows them to fully capitalize on the benefits earned through their service, positioning VA loans as not just a pathway to acquiring property but as a valuable asset in their post-service lives.