VA Loan Vs. Conventional Loan:

Not every borrower has access to the same mortgage options. However, if you are an eligible active-duty or former military service member (or their surviving spouse), you can take advantage of a VA loan.

VA loans, provided by the Department of Veterans Affairs, are notable for their affordable costs and lenient criteria compared to other home financing options. Yet, they aren’t the sole choice available. Depending on the lender and your financial situation, conventional loans might also present competitive interest rates. So, when it comes to purchasing or refinancing a property, how do you decide between a VA loan and a conventional loan?

Let’s delve into the differences between VA loans and conventional loans.

VA Loans vs. Conventional Loans: A Comparison

Both VA loans and conventional loans offer distinct features for individuals in the market for a new home.

Conventional Loan

The majority of conventional loans are conforming loans, adhering to the standards required to be bought by mortgage purchasers like Freddie Mac and Fannie Mae. On the other hand, a jumbo loan is a type of conventional mortgage that does not conform because it surpasses the borrowing limits established by Fannie Mae and Freddie Mac.

Being conforming loans, conventional mortgages are more widespread and follow a more uniform process. Since these loans can be transferred to mortgage buyers, reducing the lender’s risk, they often come with lower costs than non-conforming loans.

VA Loan

VA loans are categorized as government or non-conforming loans. As non-conforming mortgages, VA loans do not qualify for sale to Fannie Mae or Freddie Mac. Instead, government loans are sold to Ginnie Mae, a U.S. government entity that supports liquidity for government-insured loans. Non-conforming loans also encompass jumbo loans, Federal Housing Administration (FHA) loans, and U.S. Department of Agriculture (USDA) loans.

Non-conforming loans, including VA loans, typically have more flexible borrowing limits than conventional loans, making them more accessible for borrowers aiming to qualify for a mortgage.

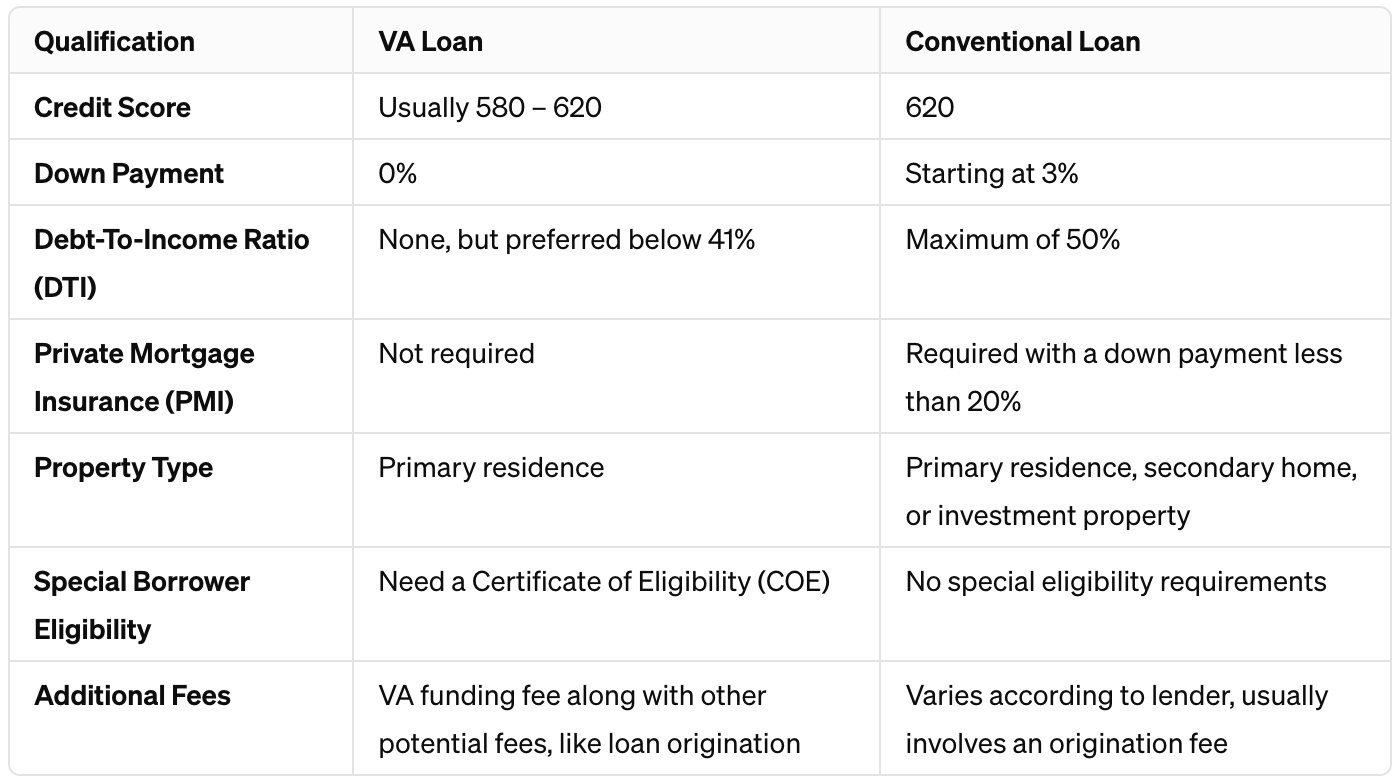

Mortgage Eligibility Criteria for VA Loans vs. Conventional Loans Although there are some similarities in the qualifications needed for VA and conventional loans, each type of mortgage has its unique set of criteria. Key factors that differentiate them include the qualification process, specific eligibility conditions, and any extra charges that may be incurred.

Below is a table to outline these essential characteristics and more for both loan categories.

Here’s the table summarizing the mortgage qualifications for VA loans versus Conventional loans:

Credit Score Requirements

Obtaining approval for a VA loan is often more straightforward than for a conventional mortgage due to the more lenient credit score criteria associated with VA loans.

The Department of Veterans Affairs does not specify a minimum credit score for VA loans; this requirement is set by the lenders that provide these loans. You might find that these lenders apply more accommodating standards compared to those for conventional mortgages. While the credit score threshold for conventional mortgages typically starts at 620, Elevation Mortgage extends VA loans to applicants with scores as low as 500.

Down Payment Considerations

A significant advantage of VA loans is their potential for no down payment requirement. Depending on your credit standing and the purchase price of the home, your lender might still ask for a down payment, especially in a competitive market scenario with several offers.

Conversely, conventional loan providers generally favor a larger initial payment, with a minimum often at 3% but suggesting 20% or more to bypass the need for mortgage insurance.

Debt-To-Income Ratio Insights

In the loan vetting process, lenders will examine your debt-to-income ratio (DTI), which is the portion of your gross monthly income that goes towards paying debts. This metric helps lenders gauge your capability to manage mortgage payments given your existing financial obligations.

While the VA is open to any DTI ratio, VA loan providers usually look for ratios under 41%. On the other hand, you might qualify for a conventional loan with a DTI up to 50%, though a lower ratio could be preferable to lenders.

The DTI is an important factor among others that lenders review during the preapproval phase of loan application.

Understanding Private Mortgage Insurance (PMI)

For conventional loans, making a down payment of less than 20% generally necessitates the addition of private mortgage insurance (PMI) to protect lenders in case of default. This requirement may also be influenced by your credit score, as both a low down payment and a low credit score are considered indicators of potential default risk.

PMI could be charged as an upfront fee at closing, an ongoing charge incorporated into your monthly payments, or a mix of both, varying by lender.

Conversely, VA loans do not require mortgage insurance, thanks in part to the absence of a mandatory down payment. Instead, the VA includes a funding fee to safeguard against defaults.

Property Eligibility Considerations

Both VA and conventional loans can be used to purchase a primary residence. However, VA loans restrict the purchase of second homes or investment properties, though they do allow for the possibility of generating rental income through a multi-unit primary residence.

While conventional loans permit the purchase of investment or secondary properties, acquiring additional property types might become more challenging due to potentially altered qualification criteria, such as the need for extra financial reserves.

Borrower Eligibility Criteria

Conventional loans rely on standard eligibility factors like income and credit score without special borrower qualifications. In contrast, VA loan eligibility is established through a Certificate of Eligibility (COE), based on meeting service requirements, being a surviving spouse of a service member who died in duty, or having an appropriate discharge status.

Loan Fees and Additional Costs

Both loan types typically involve an origination fee, usually ranging from 0.5% to 1% of the loan amount, paid during closing. While both may have this fee, VA loans limit the amount and exclude certain charges, such as prepayment penalties.

The VA Funding Fee

VA loans include a funding fee, an upfront cost varying between 1.25% and 3.3% of the loan amount, depending on prior VA loan usage and down payment size. This fee, which can be financed into the loan, helps cover the costs if a borrower defaults. Veterans receiving disability compensation are exempt from this fee.

Other Key Differences

It’s important to note other distinctions, such as VA loans not having loan limits whereas conventional loans do, set by county (most counties had a limit of $726,200 for a single-family home in 2023).

Interest rates also differ, with VA loans often offering lower rates compared to conventional loans, usually by 0.25% to 0.42%.

Moreover, the VA caps closing costs, which, combined with competitive rates, may offer financial advantages with VA loans.

Exploring the Advantages of VA Loans Compared to Conventional Loans

The perks of choosing a VA loan over a conventional loan are significant. Let’s revisit some of the key benefits that VA loans offer:

- Zero Down Payment: One of the standout features of VA loans is that they do not require a minimum down payment, allowing you to purchase a home without upfront investment.

- No Mortgage Insurance: Unlike conventional loans, opting for a VA loan means you won’t need to pay private mortgage insurance (PMI), even with no down payment.

- Favorable Terms: With the backing of the government, VA loans present less risk to lenders in case of default, leading to more favorable terms for borrowers. This often translates into lower interest rates and other beneficial aspects.

In essence, VA loans offer a more accommodating approval process and come with several cost-saving advantages, making them an attractive option without the burden of PMI or significant down payments.

Deciding Between Loan Types: A Personal Decision

While VA loans are appealing for their cost benefits and easier approval, conventional loans may also offer attractive terms depending on the lender.

When weighing your options between VA and conventional loans, assess their requirements and see which aligns better with your circumstances. For instance, VA loans might be more suitable for first-time buyers due to easier mortgage qualifications. Conversely, if you’re aiming to buy a second home or an investment property, a conventional loan would be the necessary route.

Choosing the loan that best fits your needs is the next step, setting you on the path to understanding your qualifying amount through the mortgage application process.