If you have a lower credit score or limited savings for a down payment, an FHA loan could be a suitable option for you. These loans, supported by the Federal Housing Administration, offer the possibility of purchasing a home with a credit score as low as 580 and a down payment as minimal as 3.5%. In specific scenarios, a home purchase with a credit score of 500 is feasible, though this requires a 10% down payment.

FHA loans entail a mortgage insurance premium (MIP) as an additional safeguard for the loan. Understanding the concept of FHA MIP is crucial since it affects the overall cost over various loan terms.

What Is A Mortgage Insurance Premium?

A mortgage insurance premium is a distinct form of insurance paid on FHA loans, offering your lender protection if you fail to repay. FHA MIP benefits home buyers by potentially reducing the need for a larger down payment to secure a mortgage.

See What You Qualify For

What is the Cost of an FHA Mortgage Insurance Premium?

Your FHA loan Mortgage Insurance Premium (MIP) consists of two parts: an initial premium and a yearly payment. The total amount you pay is determined by the loan amount.

Upfront FHA MIP

The initial MIP payment amounts to 1.75% of your loan’s total value. For instance, with a $450,000 mortgage, your upfront payment would be $7,875, payable at closing or added to the loan balance. This one-time upfront payment is required, unless you refinance or secure another FHA loan later on.

Annual FHA MIP

Your yearly mortgage insurance expenses will vary based on your loan-to-value ratio (LTV), down payment size, and mortgage term length. Lenders determine your annual payment as a percentage of your base loan value.

Many FHA lenders bundle your yearly MIP into your monthly mortgage payment. To gauge your monthly costs accurately, it’s advisable to apply through your lender. Once preliminarily approved, you’ll receive a loan estimate detailing your monthly mortgage payment and annual MIP. Calculate your monthly premium by dividing the total MIP by 12. This method allows you to evaluate whether the estimated monthly payment, inclusive of your MIP, fits within your budget.

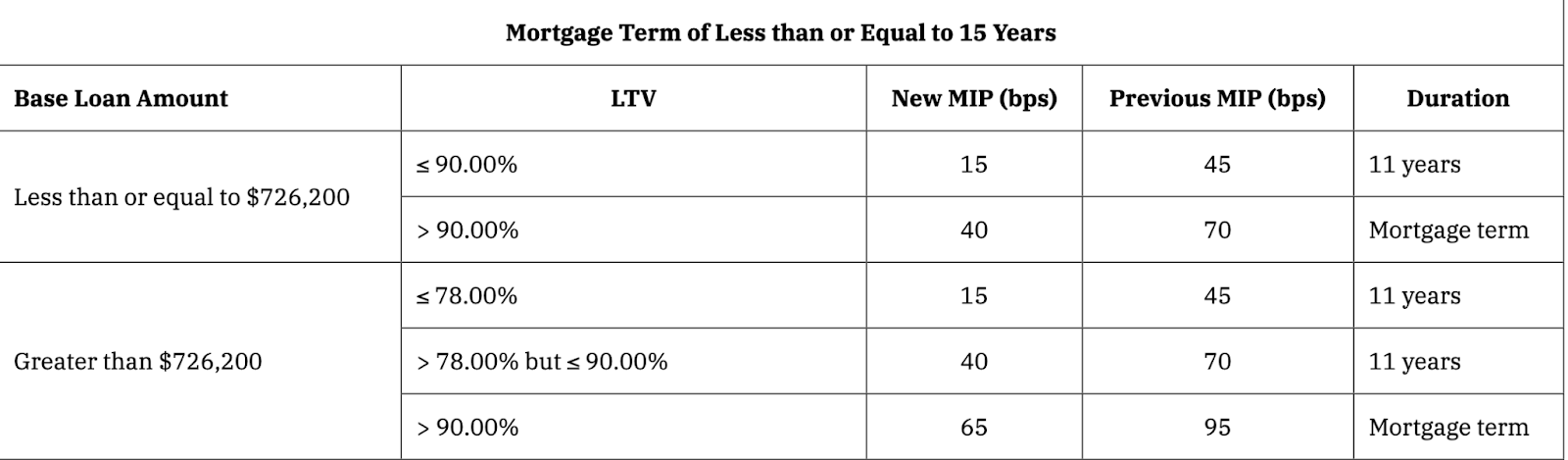

Terms of 15 years or less

Here is the anticipated cost of your yearly MIP for loan terms of 15 years or less. Consider the following scenario:

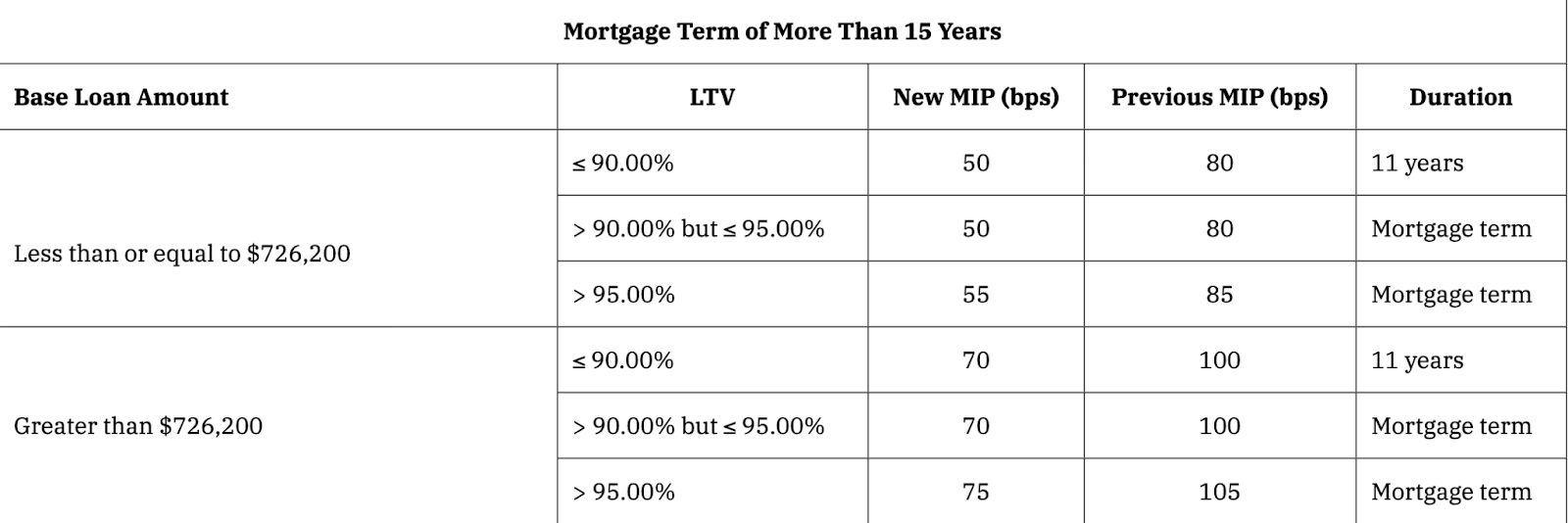

Terms Greater Than 15 Years

Below outlines the anticipated costs when opting for a loan term exceeding 15 years, with the prevalent illustration being the 30-year term. Consider the scenario where you:

What is the Duration for Paying FHA Loan Insurance?

Before 2013, MIP functioned much like PMI for conventional loans. When you hit 22% home equity, a conventional lender would automatically end your PMI.

Presently, FHA lenders don’t terminate your MIP based on equity. The duration of MIP payments hinges on your down payment. If you put down 10% or more during purchase, you’ll pay MIP for the initial 11 years. With less than 10% down, MIP payment continues for the loan’s entirety.

Is It Possible to Bypass FHA Mortgage Insurance?

To avoid paying MIP on an FHA loan, options are available to lower or discontinue payments after a few years. First-time or repeat buyers with a minimum 10% down payment can cease MIP after 11 years, or opt for a different loan type to eliminate this insurance. Homeowners can refinance from an FHA to a conventional mortgage to halt MIP payments. Delve into these strategies to determine the ideal mortgage for your needs.

Increase Your Savings for a Larger Down Payment

To reduce your MIP costs on an FHA loan, consider boosting your down payment. Bringing at least 10% to closing qualifies you for a reduced annual MIP and lowers your borrowed amount, leading to a decreased upfront premium. With a 10% down payment, MIP payments cease after 11 years. To enhance your home savings pre-loan closure, here are some effective strategies:

Consider Pursuing a Side Hustle

Living in the gig economy provides ample opportunity to supplement your income beyond your salary. By investing your time and resources wisely, you can easily generate additional funds. Delve into a side hustle to boost your savings for that down payment. Whether it’s dog walking or driving for a ridesharing service, the options are limitless.

Trim Excess Expenses from Your Budget

Do you track your monthly expenses for dining out and entertainment? If not, now is an ideal moment to create a budget and redirect surplus funds towards your down payment. Review your bank and credit card statements to identify areas where spending can be reduced. Even saving $5 weekly could give you an additional $260 by year-end.

Purchase a more affordable property.

Lenders determine your down payment based on a percentage of the total property value. Consequently, the same dollar amount translates to a larger down payment for a less pricey property. Smitten with a home at the peak of your budget? Ponder elucidating your circumstances to the seller while proposing a reduced purchase price.

Switch to a Conventional Loan by Refinancing.

Homeowners often opt for a switch to a conventional loan once they’ve gained 20% equity. With a conventional loan, there’s no MIP to pay; however, your lender may request PMI if your down payment is below 20%. You can eliminate MIP payments without transitioning to PMI by refinancing after hitting the 20% equity mark.

To transition to a conventional loan, you must meet your lender’s specific criteria. Keep in mind that conventional loan prerequisites are more stringent compared to FHA loans, so it may be necessary to enhance your borrower profile before pursuing a refinance. To qualify for a conventional loan, you must meet the following minimum requirements at a minimum:

Boosted Credit Score

To qualify, aim for a median FICO® Score of 620 or higher. Boost your credit score by paying your credit card and loan bills punctually and keeping spending in check as you develop equity.

Debt-to-Income Ratio (DTI)

To qualify for a conventional loan, your DTI ratio should be 50% or lower. Lower your DTI ratio by boosting household income or reducing debts.

Home Equity

Prior to refinancing your home, it is recommended to possess a minimum of 20% equity. Refinancing without reaching this threshold will result in the requirement of purchasing Private Mortgage Insurance (PMI) instead of Mortgage Insurance Premium (MIP). PMI tends to be pricier than MIP, hence ensuring you attain the appropriate equity level before proceeding with refinancing is crucial. If uncertain about your current equity status, consider reaching out to your lender for clarification.

Select an alternative government or non-conforming loan category.

To steer clear of MIP payments, exploring alternative government loans or non-conforming loans is advisable. Below, we’ve outlined these alternative options for your consideration.

USDA Loan

Considering a home purchase in a rural area with a median FICO® Score of 640+? Explore USDA loans! Unlike FHA loans, USDA loans skip the down payment and the need for PMI or MIP. Instead, a monthly guarantee fee is required, which costs less than the FHA monthly premium. Please note, Rocket Mortgage does not currently provide USDA loans.

VA Loan

Consider a VA loan if you’re a current or former member of the armed forces or a qualifying spouse. The Department of Veterans Affairs (VA) doesn’t set a minimum credit requirement, but most lenders do. To qualify for a VA loan through Rocket Mortgage, a minimum median FICO® credit score of 580 is necessary. With a VA loan, there’s no down payment required, and you won’t have to pay monthly mortgage insurance.

Instead, you’ll pay a one-time VA funding fee and standard closing costs, with the home needing to be your primary residence. Veterans receiving VA disability benefits and surviving spouses of veterans who died in the line of duty or due to a service-connected disability are exempt from the funding fee.

The Bottom Line

When you opt for an FHA loan, you’ll face an initial mortgage insurance premium at closing, along with an annual premium split into 12 monthly payments. The total amount hinges on your loan size and down payment. A larger down payment means lower annual costs.

MIP payments for FHA loans are non-negotiable. Yet, a down payment of 10% or more reduces the duration to 11 years. If below 10%, MIP is a lifelong commitment.

To cut MIP expenses, consider waiting until you reach 10% down before home buying. Alternatively, refinance to a conventional loan once you attain 20% equity to eliminate MIP.

When you’re prepared to apply for a mortgage or refinance, kick-start your online application today with Elevation Mortgage. A Home Loan Expert will guide you on minimizing or bypassing mortgage insurance payments.