Mortgage Calculator

Calculate your monthly payment for Conventional, FHA, VA, and USDA loans

📋 Loan Information

FHA Loan Details

Annual MIP rate varies based on loan amount, down payment, and loan term.

VA Loan Details

USDA Loan Details

🏠 Home Expenses

Your loan payment details will appear here

How to Use This Mortgage Calculator

This free mortgage calculator helps you quickly estimate your monthly mortgage payment for Conventional, FHA, VA, and USDA loans. Simply enter your purchase price, down payment, interest rate, and loan term above to see an instant, detailed breakdown of your monthly payment. In addition, the tool automatically accounts for PMI or mortgage insurance, property taxes, homeowners insurance, and HOA fees. As a result, you get a complete picture of your true monthly housing cost.

Not sure which loan type fits your situation? You can switch between loan types using the dropdown. Moreover, visit our mortgage loan programs page for a full overview of eligibility requirements for each program.

Understanding Your Monthly Mortgage Payment

Your total monthly mortgage payment is made up of several components. These are often referred to as PITI, Principal, Interest, Taxes, and Insurance. Understanding each piece is important because it helps you budget accurately and avoid surprises after closing. Additionally, knowing how each component works allows you to identify where you might be able to save money.

- Principal: The portion of each payment that reduces your outstanding loan balance. Over time, consequently, more of your payment goes toward principal and less toward interest.

- Interest: The cost of borrowing money, calculated based on your interest rate and remaining balance. In the early years of your mortgage, most of your payment goes toward interest.

- Property Taxes: Annual taxes assessed by your local government, typically collected monthly through an escrow account managed by your lender.

- Homeowners Insurance: Required coverage that protects your home and belongings against damage, fire, or liability.

- PMI or Mortgage Insurance: Required when your down payment is below 20% on a conventional loan, or on all FHA and USDA loans regardless of down payment size.

- HOA Fees: Monthly dues paid to a homeowners association if your property is within a planned community or condominium.

Mortgage Calculator: Loan Types Compared

Choosing the right loan type can significantly affect your monthly mortgage payment and your total cost over time. Therefore, it's worth understanding the key differences before you decide. Below, we compare the four loan types supported by this mortgage calculator.

Conventional Loan Mortgage Calculator

Conventional loans are the most widely used mortgage type in the United States, available with as little as 3% down. However, if your down payment is less than 20%, you'll pay Private Mortgage Insurance (PMI). PMI rates typically range from 0.17% to 1.80% annually, depending on your credit score and loan-to-value ratio. According to the Consumer Financial Protection Bureau, PMI is automatically canceled when your LTV reaches 78%, and you can request removal at 80% LTV. Learn more on our conventional loans page.

FHA Loan Mortgage Calculator

FHA loans are government-backed mortgages that are especially popular with first-time homebuyers because they require only a 3.5% down payment with a credit score of 580 or higher. In addition to the down payment, FHA loans include a 1.75% upfront Mortgage Insurance Premium (MIP) that is financed into the loan. On top of that, borrowers pay an annual MIP of 0.50% to 0.55% for most scenarios. If your down payment is less than 10%, MIP is required for the life of the loan. Conversely, with 10% or more down, MIP is removed after 11 years. For full details, visit our FHA loans page.

VA Loan Mortgage Calculator

VA loans are exclusively available to eligible veterans, active-duty service members, and surviving spouses. They offer no down payment and no PMI, making them one of the most powerful mortgage options available. A VA funding fee of 1.40% to 3.30% applies unless the borrower is exempt due to a service-connected disability. Moreover, the funding fee varies depending on whether it is a first or subsequent use of the VA loan benefit. Verify your eligibility through the U.S. Department of Veterans Affairs, or see our VA loans guide for full details.

USDA Loan Mortgage Calculator

USDA loans are designed for homebuyers in eligible rural and suburban areas and, like VA loans, require no down payment. USDA loans include a 1.0% upfront guarantee fee and a 0.35% annual fee paid for the life of the loan. It's worth noting that income limits apply based on your county and household size, so not all buyers will qualify. As a result, you should check property and income eligibility using the USDA eligibility tool. For more information, visit our USDA loans page.

How the Mortgage Calculator Formula Works

This mortgage calculator uses the standard loan amortization formula: M = P × [r(1 + r)^n] / [(1 + r)^n – 1]. In this formula, M is your monthly principal and interest payment, P is the total loan amount (including any financed upfront fees such as FHA MIP or VA funding fee), r is the monthly interest rate (annual rate divided by 12), and n is the total number of monthly payments. For example, on a 30-year mortgage, n equals 360 payments.

In addition to principal and interest, the mortgage calculator adds your estimated property taxes, homeowners insurance, PMI or mortgage insurance, and HOA fees to produce your total monthly mortgage payment. Consequently, the figure shown in the results is your true all-in housing cost — not just the loan payment itself.

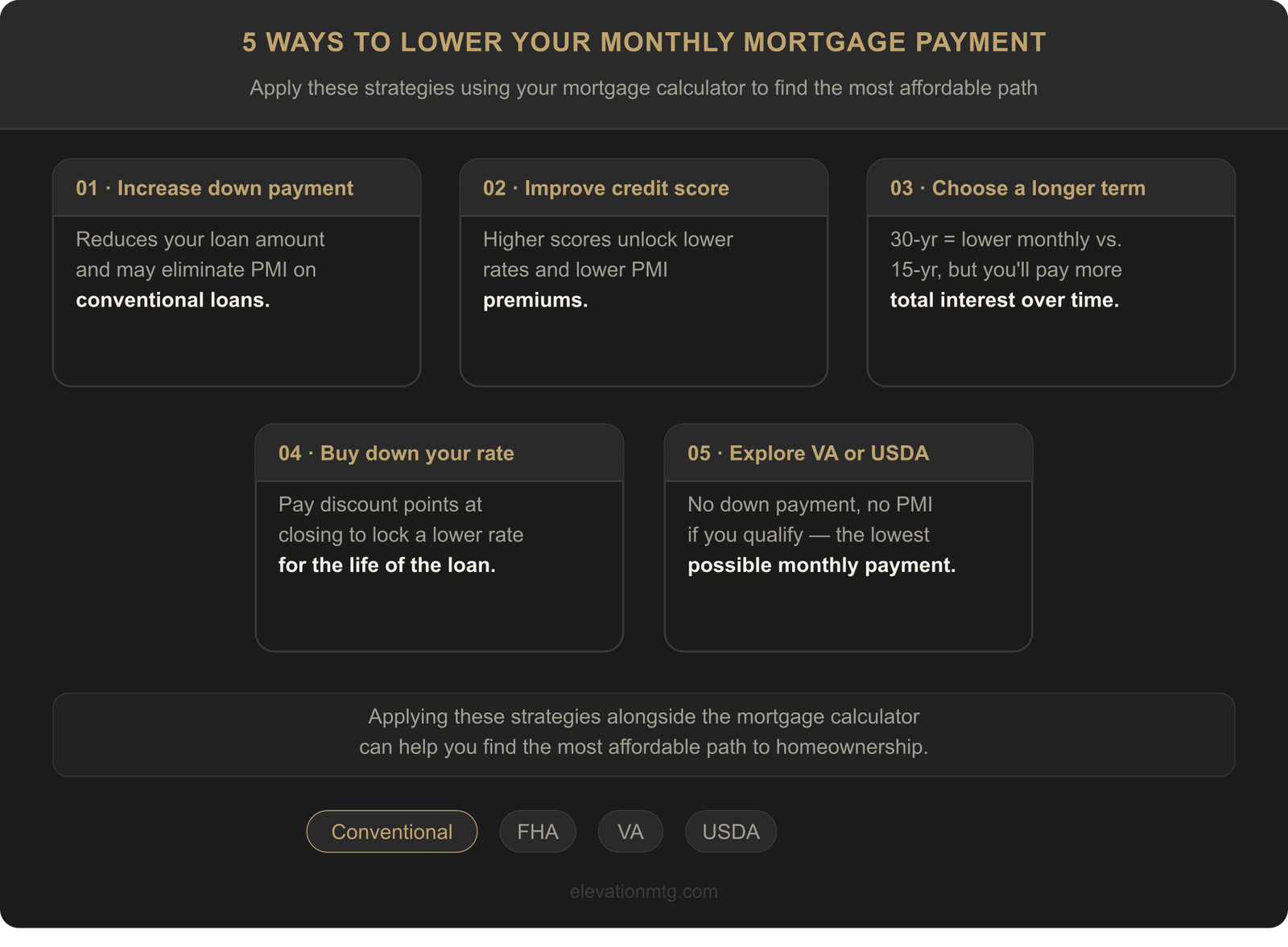

Tips to Lower Your Monthly Mortgage Payment

If your mortgage calculator result is higher than your budget allows, there are several effective strategies you can use to reduce your monthly payment:

- Increase your down payment — A larger down payment directly reduces your loan amount and, in turn, may eliminate the need for PMI altogether on a conventional loan.

- Improve your credit score before applying — Higher scores qualify you for lower interest rates and lower PMI rates, which means significant long-term savings.

- Choose a longer loan term — A 30-year term produces a lower monthly payment than a 15-year term. However, keep in mind that you'll pay more total interest over time.

- Buy down your interest rate — Paying discount points at closing lowers your rate and consequently reduces your monthly mortgage payment for the life of the loan.

- Explore VA or USDA loans — If you qualify, these programs offer no down payment and no PMI, which can result in substantially lower monthly payments compared to conventional or FHA options.

If you're self-employed or have non-traditional income, qualifying for a mortgage may require additional documentation. In that case, learn about options available for self-employed and complex income borrowers. Additionally, if you already have a mortgage and rates have dropped, visit our mortgage refinance page to explore whether refinancing could save you money.

Mortgage Calculator FAQ

How much house can I afford based on the mortgage calculator?

A widely used guideline is that your total monthly housing payment — including principal, interest, taxes, insurance, PMI, and HOA fees — should not exceed 28% to 33% of your gross monthly income. For example, if your household earns $7,000 per month, your target payment range would be between $1,960 and $2,310. Therefore, use the mortgage calculator above to test different purchase prices and down payment amounts until you find a payment that fits comfortably within that range. The CFPB explains how lenders evaluate debt-to-income ratios when determining how much you can borrow.

What is an amortization schedule and how does the mortgage calculator use it?

An amortization schedule is a complete table showing how each monthly payment is divided between principal and interest over the full life of your loan. In the early months, most of your payment goes toward interest. However, as the balance decreases, a progressively larger share goes toward principal. As a result, you build equity faster in the later years of your mortgage. Click the "Show Amortization Schedule" button in the mortgage calculator above to view your full schedule — either annually or month by month.

When can I remove PMI from my mortgage?

For conventional loans, PMI is automatically canceled when your loan-to-value ratio reaches 78% of the original purchase price based on your amortization schedule. In addition, you have the right to request cancellation once your LTV reaches 80%. On the other hand, for FHA loans with less than 10% down, MIP remains for the life of the loan and can only be removed by refinancing into a conventional mortgage. Meanwhile, VA loans never carry PMI — which is one of their most significant financial advantages.

What credit score do I need to qualify for the loan types shown in this mortgage calculator?

Credit score minimums vary by loan type. Conventional loans typically require a score of 620 or higher, though scores of 740 or above unlock the best rates and lowest PMI costs. FHA loans accept scores as low as 580 with a 3.5% down payment, or alternatively 500 with a 10% down payment. VA loans have no official government-set minimum, although most lenders require at least 620. Finally, USDA loans generally require a score of 640 or above. In general, the higher your credit score, the lower your interest rate and overall mortgage cost will be. Therefore, if your score needs improvement, it's often worth waiting a few months before applying.

Advertising Disclosure. The down payment percentages shown in the program comparison table above are minimum advertised figures and constitute trigger terms under the Truth in Lending Act (TILA) / Regulation Z. Accordingly, the following full disclosures apply by program. A lender underwriting fee of $1,095 applies to all examples below and is included in each APR calculation as a finance charge. Conventional: Based on a purchase price of $412,371 with a down payment of $12,371 (3%), the base loan amount is $400,000. Interest rate: 6.500%. APR: 6.527%. Loan term: 30 years (360 monthly payments). Estimated monthly principal and interest payment: $2,528. Credit score assumed: 740. Private mortgage insurance (PMI) is not included in this payment and would be required with less than 20% down, increasing the monthly obligation. PMI is removable once the borrower reaches 20% equity. FHA: Based on a purchase price of $300,000 with a down payment of $10,500 (3.5%), the base loan amount is $289,500. An upfront mortgage insurance premium (MIP) of 1.75% ($5,066) is financed into the loan, bringing the total loan amount to approximately $294,566. Interest rate: 6.500%. APR: 6.653%. Loan term: 30 years (360 monthly payments). Estimated monthly principal and interest payment: $1,862. An annual MIP of approximately $135 per month is also required and is not included in the P&I payment shown. Credit score assumed: 610. VA: Based on a purchase price of $400,000 with no down payment, the base loan amount is $400,000. A VA funding fee of 2.15% ($8,600) is financed into the loan, bringing the total loan amount to approximately $408,600. Interest rate: 6.500%. APR: 6.527%. Loan term: 30 years (360 monthly payments). Estimated monthly principal and interest payment: $2,583. No private mortgage insurance (PMI) is required on VA loans. The funding fee may vary based on down payment amount, loan type, and whether the borrower has previously used VA loan benefits. Certain veterans may be exempt from the funding fee. No published credit score minimum; lender overlays may apply. USDA: Based on a purchase price of $400,000 with no down payment, the base loan amount is $400,000. An upfront guarantee fee of 1% ($4,000) is financed into the loan, bringing the total loan amount to approximately $404,000. Interest rate: 6.500%. APR: 6.516%. Loan term: 30 years (360 monthly payments). Estimated monthly principal and interest payment: $2,554. An annual fee of approximately $118 per month is also required and is not included in the P&I payment shown. Credit score assumed: 640 (typical). USDA loans are subject to geographic eligibility and income limits. For all programs: Taxes, homeowner's insurance, and any applicable HOA fees are not included in the payment estimates shown above. Rates and terms are subject to change without notice. Not all applicants will qualify. This is not a commitment to lend. Loan approval is subject to credit approval, income verification, appraisal, and program eligibility at the time of application. Down payment requirements, credit score minimums, and program availability vary by loan type and lender overlay.