Mortgage Approval Factors

You've done some reading on mortgage approval factors. You have a rough sense of what's involved in getting a mortgage.

Now you want to know: based on the mortgage approval factors lenders actually care about, where do you stand?

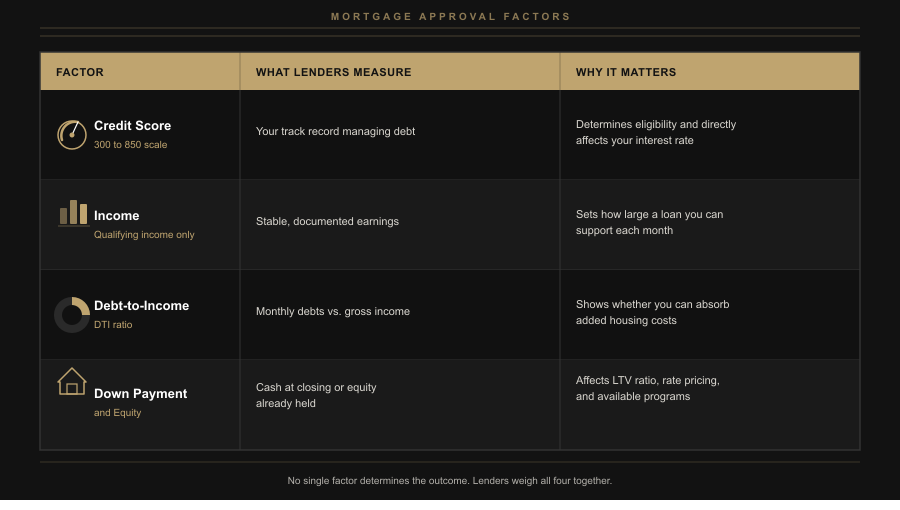

The answer comes down to four things: 1. your credit score, 2. your income, 3. your debt-to-income ratio, and 4. how much you're putting down. No single number determines the outcome. Lenders weigh these factors together, and how they interact matters as much as any individual metric.

Let's break down each factor. What it is, how lenders use it, and what the realistic ranges look like so you can figure out whether you're ready to have a real conversation or whether there's something worth addressing first.

The Four Mortgage Approval Factors at a Glance

Mortgage Approval Factor #1: Credit Score

Lenders pull a FICO score — not the free score from your banking app, which often uses a different scoring model — to assess how reliably you've managed debt. According to myFICO's credit education resources, FICO scores range from 300 to 850. Most mortgage programs require a minimum somewhere in the mid-600s, but the score that gets you approved and the score that gets you the best rate are two separate benchmarks.

FHA loans allow scores as low as 580 with a 3.5% down payment — or as low as 500 with 10% down. Conventional loans typically require a minimum of 620, though borrowers below 680 may face higher rates or added conditions.

| Credit Score Range | Typical Impact on Your Mortgage |

|---|---|

| 760+ | Best available rates — strongest pricing across most loan types |

| 720–759 | Strong — competitive rates, most programs available |

| 680–719 | Good — minor rate adjustments may apply on conventional loans |

| 640–679 | Eligible but limited — higher rate, fewer program options |

| 580–639 | FHA-eligible — conventional approval unlikely without strong compensating factors |

| Below 580 | Difficult — very limited options; credit rebuilding typically needed first |

One thing to keep in mind: your score at the time you apply is what counts. If you've recently paid down balances or corrected errors on your report, those changes can show up within a billing cycle or two.

Mortgage Approval Factor #2: Income

Lenders aren't just asking how much you earn. They're asking whether that income is stable, documented, and likely to continue. A salaried employee with two years at the same company is straightforward to evaluate. A consultant who had a strong year followed by a slow one takes more analysis — but isn't disqualified.

What Types of Income Count?

Most lenders will consider: base salary or hourly wages, overtime and bonuses (typically averaged over 24 months), self-employment income (net, not gross), rental income, retirement or Social Security income, alimony or child support (if it will continue for at least three years), and certain asset-based income.

The phrase that matters in lending is "qualifying income" — income that's both documented and stable enough for a lender to count on. If you're self-employed or have income that doesn't show up cleanly on a W-2, that doesn't disqualify you. The documentation process is just different, and our page on self-employed and complex income situations gets into those specifics.

How Much Income Do You Need?

There's no set dollar amount. What matters is the ratio of your income to your debts and proposed housing costs — which brings us to DTI.

Mortgage Approval Factor #3: Debt-to-Income Ratio

Your debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward monthly debt payments. Lenders calculate it two ways:

- Front-end DTI: Just your proposed housing payment (principal, interest, taxes, insurance, HOA if applicable) divided by gross monthly income

- Back-end DTI: All monthly debt payments — housing plus car loans, student loans, credit cards, and anything else — divided by gross monthly income

Back-end DTI is what lenders focus on. Per Fannie Mae guidelines, the standard limit for a conventional loan is 45%, though automated underwriting systems can approve DTIs up to 50% when the rest of the file is strong — high credit score, cash reserves after closing, or a larger down payment. FHA loans generally allow back-end DTIs up to 43–50% depending on compensating factors.

A common mistake people make when estimating their own DTI: they forget to include minimum credit card payments and student loan payments. Even if you pay more than the minimum each month, lenders use the minimum payment listed on your credit report. Our mortgage calculator can help you get a rough sense of how DTI plays out at different price points.

Mortgage Approval Factor #4: Down Payment and Equity

How much you put down shapes your loan options, your interest rate, and your monthly payment for years to come. But the 20% figure that many buyers carry in their heads is not a requirement — it's one threshold among several.

According to the National Association of Realtors' 2023 Profile of Home Buyers and Sellers, the median down payment for first-time homebuyers was 8%, and repeat buyers put down a median of 19%. Several loan programs allow even less:

- FHA loans: 3.5% minimum (with a 580+ credit score)

- Conventional loans: 3–5% minimum (with private mortgage insurance)

- VA and USDA loans: 0% down for eligible borrowers

- Jumbo loans: Typically 10–20% minimum

Putting less than 20% down on a conventional loan means you'll pay private mortgage insurance (PMI), which is added to your monthly payment until you reach 20% equity. That's a real cost, but for many buyers it makes more financial sense to buy now with PMI than to wait years saving a larger down payment while prices and rates shift.

For homeowners refinancing rather than buying, equity plays the same role. Lenders typically want at least 5–20% equity remaining after a refinance, depending on the loan type and transaction. Our mortgage refinance page covers how that works.

How These Mortgage Approval Factors Work Together

No lender evaluates these factors in isolation. A strong credit score can sometimes offset a higher DTI. A large down payment can compensate for a thinner credit history. This is why two people with the same income might qualify for very different loan amounts — or why someone with a 700 credit score might get a better deal than someone at 690, depending on everything else in the file.

Lenders run your application through automated underwriting systems — Fannie Mae's Desktop Underwriter (DU) or Freddie Mac's Loan Product Advisor (LPA) — that weigh all of these factors together and return an approval recommendation. That recommendation isn't the final word, but it's a strong signal of where you stand and which programs fit.

What This Looks Like in Practice

A buyer in Colorado — we'll call her Dana — came to us with a 682 credit score, steady W-2 income of $78,000/year, about $22,000 saved for a down payment, and $520/month in existing debt payments from a car loan and student loans.

At a purchase price of $375,000 with 8% down ($30,000, supplemented by gift funds from family), her back-end DTI came out to roughly 44%. Her score made a conventional loan possible, though she wasn't in the best pricing tier. We ran her through both conventional and FHA scenarios — FHA carried a lower rate for her score range, but the upfront and annual mortgage insurance premiums added cost over the life of the loan.

After walking through both options side by side, she chose conventional with a plan to drop PMI once she hit 20% equity. No single factor made her application strong or weak. It was the full picture — and understanding the trade-offs between programs — that led to a loan she felt confident about.

Is This Page Right for Where You Are Right Now?

✓ This is useful if you're...

- Trying to gauge whether you'd qualify before talking to anyone

- Wanting to understand a past denial or high rate quote

- Planning to buy in the next 6–18 months and want to know what to work on

- Comparing loan programs and unsure which fits your financial picture

✗ A different starting point might be better if...

- You're already under contract and need a fast pre-approval

- You know your numbers and want to compare specific loan programs — our loan programs overview is more direct

- Your income situation is complex enough that a 15-minute phone call will answer more than any page can

Get Honest Answers From Someone Who Knows

You've read enough to have a sense of where you might stand. A real conversation with a loan officer will fill in the gaps — and it doesn't commit you to anything.

Ask a Real QuestionFAQs: Mortgage Approval Factors

It depends on the loan type. FHA loans allow scores as low as 580 with 3.5% down. Conventional loans typically require a minimum of 620, though scores below 680 often come with higher rates or tighter conditions. For the best pricing on conventional loans, you generally want a score of 740 or above. The score you need to get approved and the score that gives you the best rate are two different things.

Divide your total monthly debt payments by your gross monthly income (before taxes). Lenders look at two versions: front-end (just the housing payment) and back-end (all debts including housing). Back-end DTI is what typically determines eligibility. For most conventional loans, lenders prefer back-end DTI below 45%, though automated underwriting systems sometimes approve up to 50% when compensating factors like strong credit or cash reserves are present.

Yes — not because one type is better, but because each is documented and averaged differently. W-2 employees are the most straightforward. Self-employed borrowers typically need two years of tax returns and business documents, and qualifying income is based on net income after deductions — which can be significantly lower than what was actually earned. Hourly and commission earners may have variable income averaged over 24 months. If any of this applies to you, our page on complex income situations goes deeper.

No. The 20% figure is the threshold where private mortgage insurance (PMI) is no longer required on conventional loans. But many buyers put down 3–10% and carry PMI until they build equity. FHA loans require 3.5% down for borrowers with a 580+ credit score. VA and USDA loans allow 0% down for eligible borrowers. Less down means a higher monthly payment and PMI costs, but it's a legitimate and common path — and often makes more sense than delaying a purchase for years.

Often, yes — within limits. Automated underwriting systems evaluate the full picture. A higher credit score can sometimes support a higher DTI. A large down payment can offset thinner credit history. Strong cash reserves after closing can also help borderline applications. That said, every loan program has hard minimums — a credit score floor, a maximum DTI ceiling — that can't be compensated away. A loan officer can tell you quickly whether your specific mix of factors works, and with which programs. The CFPB's homebuying resources are also a solid reference for understanding how the broader process fits together.

Mortgage Approval Factor Disclaimer

Representative example only. "Dana" is a fictional name used to illustrate a real borrower profile. Financial details have been generalized to protect privacy. DTI calculation includes estimated property taxes, homeowner's insurance, and PMI based on assumed rates and may differ from actual figures. Gift fund eligibility varies by loan program and lender guidelines. PMI cancellation is subject to lender policies, applicable law, and achievement of required equity thresholds — automatic cancellation generally occurs at 78% LTV under the Homeowners Protection Act, though borrower-requested cancellation may be available at 80% LTV. Conventional and FHA loan comparisons are program-specific and will vary based on credit score, loan amount, down payment, and market conditions at time of application. Results are not guaranteed. Not all borrowers will qualify.