Home Loan Timeline

How Fast Can You Close?

The home loan timeline at most big banks runs 45–60 days. That has more to do with internal bureaucracy and staffing layers than with how long the process actually needs to take. As a mortgage broker, Elevation Mortgage closes most loans in 21 days — and rarely goes beyond 30, even on more complex files.

The difference isn't magic. It's fewer layers between your file and a decision. When a big bank underwrites in-house and routes your file through multiple departments, each hand-off costs days. We work with multiple lenders simultaneously, move files directly, and our processors don't carry the kind of backlog that slows institutional lenders down.

Select your loan type below to see exactly how the home loan timeline works — phase by phase, with real timeframes.

Select Your Loan Type

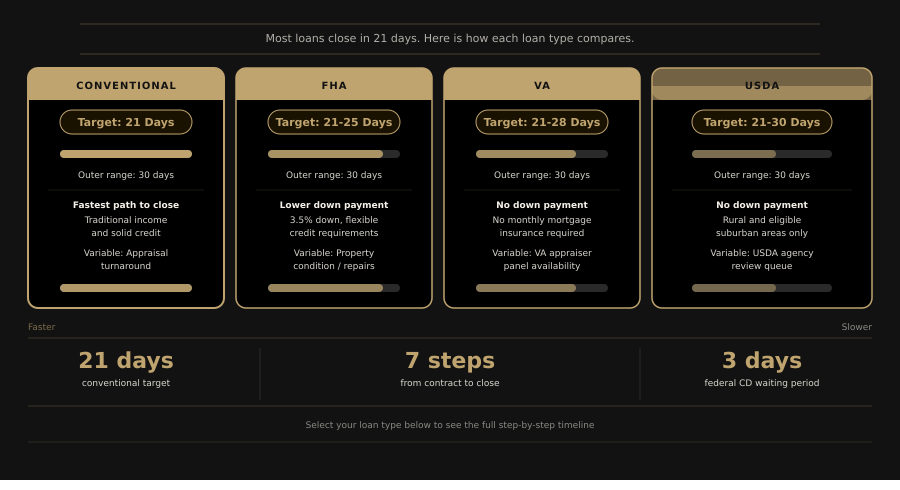

Conventional Loan Timeline — Target: 21 Days

-

1

Pre-ApprovalDay 1

We collect everything upfront — pay stubs, W-2s, bank statements, tax returns, and ID. By the time you're under contract, your file is already organized and ready to submit. We issue pre-approval the same day in most cases. This is the step that sets the pace for everything that follows.

-

2

Under Contract — Appraisal Ordered ImmediatelyDay 1–2

The moment you're under contract, we order the appraisal. There's no waiting on paperwork or internal approvals. The appraisal runs concurrently with underwriting — we don't wait for one to finish before starting the other.

-

3

File Submitted to UnderwritingDay 2–3

Because we collected documents at pre-approval, your complete file goes to underwriting within 24–48 hours of going under contract. We chase nothing down at this stage — it's already in hand.

-

4

Underwriting Decision1–3 Days Per Submission

Our underwriters turn decisions in 1–3 business days. If the underwriter returns conditions, we respond fast — we clear most conditions in a day or two. Clean files with no credit or income surprises often come back approved with minimal conditions.

-

5

Appraisal ReturnedDays 5–10 (Concurrent)

Appraisals typically return within 5–10 days. Because this runs parallel to underwriting, it rarely adds time to the overall clock. If the appraisal returns while underwriting is still in review, both are ready at the same time.

-

6

Clear to Close + Closing Disclosure1–2 Days After Conditions Cleared

Once all conditions are satisfied, we issue the clear to close and send the Closing Disclosure the same day. Federal law requires a 3-business-day waiting period after the Closing Disclosure is delivered before you can sign — that's a consumer protection rule, not a lender delay. We get the CD out the moment we're clear so that clock starts immediately.

-

7

Closing DayDay 17–21

You sign, funds are wired, ownership transfers. For a well-organized conventional file, closing at or before day 21 is routine for us.

FHA Loan Timeline — Target: 21–25 Days

-

1

Pre-ApprovalDay 1

FHA pre-approval requires the same document package as conventional — collected in full on day one. We review your file against FHA guidelines during pre-approval so there are no surprises in underwriting. FHA has specific rules around credit history, gift funds, and employment gaps, and we address all of that upfront.

-

2

Under Contract — FHA Appraisal OrderedDay 1–2

We order the FHA appraisal immediately at contract. FHA appraisals go beyond value — the appraiser also checks that the property meets HUD's minimum property standards. Things like peeling paint, exposed wiring, or missing handrails can trigger repair requirements. We flag any known property concerns with buyers before they go under contract so it's not a surprise.

-

3

File Submitted to UnderwritingDay 2–3

Your complete file — already assembled at pre-approval — goes to the FHA-approved underwriter within 48 hours of contract. No scrambling for documents at this stage.

-

4

Underwriting Decision1–3 Days Per Submission

FHA underwriting decisions come back within 1–3 business days. Conditions are typical and usually addressable quickly. If the appraisal flagged property repairs, that's where an FHA timeline can stretch — seller cooperation on repairs is the variable, not our process.

-

5

Appraisal ReturnedDays 5–12 (Concurrent)

FHA appraisals return in roughly the same timeframe as conventional. Again, this runs concurrently — not sequentially — with underwriting.

-

6

Clear to Close + Closing Disclosure1–2 Days After Conditions Cleared

We issue CTC within 1–2 days of clearing conditions. The Closing Disclosure goes out the same day, starting the required 3-business-day federal waiting period.

-

7

Closing DayDay 18–25

On a property with no condition issues, FHA closes right alongside conventional. The extra days in the FHA range come from appraisal repair situations — when the property is in good shape, the timeline holds.

VA Loan Timeline — Target: 21–28 Days

-

1

Certificate of Eligibility + Pre-ApprovalDay 1

We pull your Certificate of Eligibility (COE) electronically through the VA portal — most come back within minutes. This happens the same day as pre-approval. We collect all documents at this stage: military pay stubs or retirement statements, DD-214 if applicable, bank statements, and tax returns. No VA loan should start without the COE in hand.

-

2

Under Contract — VA Appraisal OrderedDay 1–2

We order the VA appraisal immediately. VA appraisals must go to a VA-assigned appraiser from the regional panel — neither you nor your lender can choose who handles it. In most markets, the report comes back within 7–12 days. In rural areas, appraiser availability can stretch that window.

-

3

File Submitted to UnderwritingDay 2–3

Your fully assembled file goes to VA underwriting within 48 hours of contract. VA underwriting reviews income, residual income (a VA-specific metric that looks at what's left after debts and housing costs), credit, and the appraisal once it's in.

-

4

Underwriting Decision1–3 Days Per Submission

VA underwriting turnaround is 1–3 business days with us. We handle residual income calculations and VA-specific income documentation upfront so there are no surprises at this stage.

-

5

VA Appraisal ReturnedDays 7–14 (Concurrent)

VA appraisals also check Minimum Property Requirements (MPRs) — similar to FHA. If repairs are required, that's a negotiation with the seller and can add a few days. A property in good condition clears this step without issue.

-

6

Clear to Close + Closing Disclosure1–2 Days After Conditions Cleared

We issue CTC within 1–2 days, and the Closing Disclosure goes out the same day. The federal 3-business-day waiting period applies here as with all loan types.

-

7

Closing DayDay 18–28

VA loans carry no down payment requirement and no monthly mortgage insurance — and they close fast when the file is clean and the property is in good shape. The VA funding fee typically rolls into the loan.

USDA Loan Timeline — Target: 21–30 Days

-

1

Eligibility Check + Pre-ApprovalDay 1

Before anything else, we confirm two things: the property sits in a USDA-eligible rural area, and your household income falls within USDA limits for that county. Both checks take minutes. If you qualify, pre-approval happens the same day — all documents collected upfront, same as every other loan type we do.

-

2

Under Contract — Appraisal OrderedDay 1–2

We order the appraisal immediately at contract. USDA appraisals must go to an approved USDA appraiser and include basic property condition standards — similar to FHA's minimum property requirements.

-

3

File Submitted to Lender UnderwritingDay 2–3

Your complete file goes to our underwriting team within 48 hours. USDA underwriting involves an additional check: household income verification for all household members, not just borrowers on the loan. We handle this at pre-approval so it doesn't slow down the underwriting stage.

-

4

Lender Underwriting Decision1–3 Days Per Submission

Our lender underwriting turn time is the same: 1–3 business days. We clear conditions quickly. Once our underwriting is complete and the appraisal is back, the file moves to the next step.

-

5

USDA Rural Development Agency Review5–7 Additional Days

This is what separates USDA from every other loan type — and it has nothing to do with how fast we work. After lender underwriting is complete, the entire file goes to the USDA Rural Development office for their own independent review. Processing times at the agency level vary by state and season. According to the USDA Rural Development program office, agency review typically adds 5–7 days to the timeline. We submit to USDA the moment lender underwriting is complete and follow up actively, but this queue is outside our control.

-

6

USDA Conditional Commitment + CTC1–2 Days After USDA Approval

Once USDA issues their Conditional Commitment, we clear any remaining lender conditions and issue the clear to close. The Closing Disclosure goes out the same day, starting the 3-business-day federal waiting period.

-

7

Closing DayDay 21–30

USDA loans offer no down payment and a low upfront guarantee fee rolled into the loan, with a low annual fee. The longer timeline is a trade-off for those benefits. We're upfront about this with every USDA borrower so your purchase contract reflects the real close date — no surprises for you or the seller.

Home Loan Timeline By Loan Types

| Loan Type | Our Target | Outer Range | Biggest Variable |

|---|---|---|---|

| Conventional | 21 days | 30 days | Appraisal turnaround |

| FHA | 21–25 days | 30 days | Property condition / appraisal repairs |

| VA | 21–28 days | 30 days | VA appraiser panel availability |

| USDA | 21–30 days | 30 days | USDA Rural Development agency review queue |

Why a Mortgage Broker Closes Faster Than a Bank

Fewer Layers. Faster Decisions.

When you apply at a big bank, your file sits in a queue alongside thousands of others. Their underwriters work on a first-in, first-out basis across their entire loan volume. Their processors manage enormous pipelines. Every internal hand-off costs time.

As a broker, we work differently:

- We collect your full document package at pre-approval — so your file is submission-ready the day you go under contract

- We access multiple lenders and route your file to the one with the fastest current turn times

- Our processors carry tighter pipelines and move conditions within hours, not days

- We order the appraisal the same day you're under contract — no waiting on internal approvals

- We issue the Closing Disclosure the moment we're cleared — starting your 3-day federal waiting period immediately

According to the Consumer Financial Protection Bureau, the average mortgage close takes 30–60 days nationally. Most of that extra time isn't the process — it's the pipeline. We've built our process to cut it down.

Home Loan Timeline Hiccups

We control our piece of the process tightly. A few things can add days regardless of lender:

- Appraisal backlog — In competitive markets, appraisers book out. We order fast and track closely, but can't control the appraiser's calendar.

- Property condition issues — FHA and VA appraisers flag problems that require repairs before closing. The seller has to agree to make them.

- Title complications — Old liens or ownership disputes in the title search take time to clear, regardless of how fast we move.

- Borrower changes mid-process — A new credit account, a job change, or an unexplained large deposit during the process can require re-underwriting. Avoid all financial changes once you're under contract.

- Homeowners Insurance — Don't wait to shop for homeowner's insurance — carriers are exiting specific markets, and a last-minute coverage gap can delay your closing.

- USDA agency queue — The only step we can't compress. See the USDA tab above.

What a 21-Day Close Actually Looks Like

A buyer in Colorado Springs came to us pre-shopping — she had a conventional loan pre-approval from her bank and expected a 45-day timeline. She called us to compare. We walked her through our process, collected her documents during that first call, and issued a pre-approval the same day.

She went under contract three weeks later. We ordered the appraisal within hours. The appraiser returned the report on day 9. Underwriting reviewed the full file — assembled at pre-approval — and came back with a conditional approval on day 11. We cleared conditions on day 13. The Closing Disclosure went out day 14, starting the 3-day federal waiting period. She signed on day 18.

Her agent had never seen a close that fast. The seller was thrilled. And she moved in 27 days before her old lease expired.

If you want to estimate your monthly payment before the conversation, our mortgage payment calculator is a good place to start.

Ready to Talk? We're Real People.

You probably have a few questions about your specific situation — your loan type, your timeline, your contract date. Our loan officers can give you a straight answer in one conversation, not a generic estimate from a form. No pressure, no application required to have the talk.

Talk to a Real Loan OfficerFAQs Home Loan Timeline

Yes — for conventional and FHA loans on properties in good condition, with a borrower who has their documents ready, 21 days is a realistic and repeatable target. The key is collecting everything at pre-approval so the file is ready to submit to underwriting the moment you're under contract. The mandatory 3-business-day waiting period after the Closing Disclosure is the one step fixed by federal law — everything before it moves on our timeline.

Large banks process enormous loan volumes through the same internal pipelines. Underwriting queues at major institutions regularly run 10–15 business days or more. Their processors manage large files with less flexibility to prioritize. As a broker, we work with multiple lenders and route your file where it moves fastest — and our processors carry tighter pipelines with faster turn times.

Federal law (specifically TRID — the TILA-RESPA Integrated Disclosure rule) requires that you receive your Closing Disclosure at least 3 business days before closing. This is a consumer protection requirement, not a lender delay. We send the Closing Disclosure the same day we issue the clear to close, so that 3-day clock starts as early as possible.

Yes. Conventional loans are fastest. FHA and VA add property condition requirements through the appraisal that can add a few days if repairs are needed. USDA is the outlier — an independent agency review by USDA Rural Development adds days that no lender can compress, regardless of their internal speed. If timeline is your top priority, talk to us about whether a conventional loan might be a better fit than a government-backed program.

The biggest thing: respond to document requests within 24 hours. Make no new financial moves — no new credit accounts, no large deposits you can't explain, no job changes — between pre-approval and closing. Confirm your homeowner's insurance binder is ready before we ask for it. And stay in contact with your loan officer rather than waiting to hear from them. An organized borrower is the difference between a 21-day close and a 35-day close.

Important Disclosures

Elevation Mortgage LLC | NMLS# 2179191 | nmlsconsumeraccess.org

This page is provided for educational and informational purposes only and does not constitute an advertisement for credit, a commitment to lend, or a guarantee of loan approval. All loan programs, eligibility requirements, and closing timelines are subject to change without notice and may vary based on borrower qualifications, property type, market conditions, and lender guidelines.

Closing timelines referenced on this page (including the 21-day target) represent typical scenarios for well-qualified borrowers with complete documentation on properties in good condition. Individual results will vary. Actual closing timelines depend on factors including but not limited to appraisal turnaround, title search results, borrower responsiveness, property condition, and third-party agency review queues (such as USDA Rural Development).

Pre-approval is not a commitment to lend. A pre-approval is based on a preliminary review of creditworthiness and does not guarantee final loan approval. Final approval is subject to underwriting review, appraisal, title clearance, and verification of all information provided.

Elevation Mortgage LLC is licensed to originate mortgage loans in Colorado and Florida. Licensing information is available at nmlsconsumeraccess.org.

Ⓡ Equal Housing Opportunity. We do business in accordance with the Fair Housing Act and the Equal Credit Opportunity Act.