Cost of Waiting to Buy a Home in Florida

Florida's housing market has shifted meaningfully over the past year. Prices are below their 2024 peak, inventory is up, and buyers currently have more negotiating leverage than they've had since before 2020. For Florida buyers, the cost of waiting isn't primarily about appreciation pressure — it's about a window of favorable conditions that is tied directly to where rates are right now, and what happens when they move.

This page provides an honest look at where Florida prices actually stand and why today’s "higher-rate" environment may actually be more favorable for your long-term wealth than the high-competition market that follows a rate drop. Use the calculator below to replace the uncertainty of waiting with a clear comparison of your options.

What the Colorado Market Is Actually Doing

Colorado's market has cooled from its 2020–2022 surge, but it hasn't stopped moving. Prices are still appreciating — just at a more measured pace. Inventory is up, buyers have more negotiating room than they've had in years, and the long-term fundamentals remain strong.

The near-term forecast is 1–4% annual appreciation — well below the pandemic peak, but still moving in one direction. That matters when you're calculating what a year of waiting actually costs.

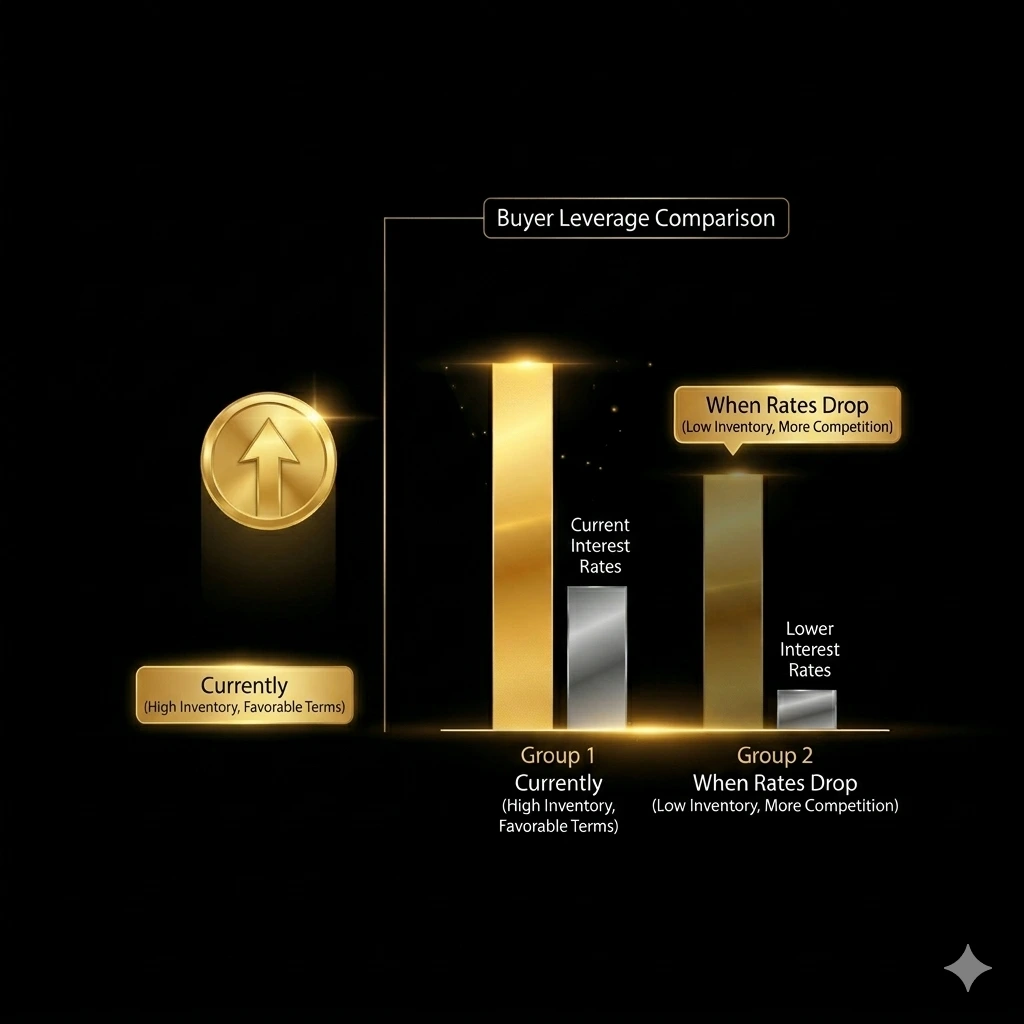

The Trade-Off Nobody Talks About: Rates vs. Prices

The most common reason Colorado buyers wait: "I'm holding off until rates come down." Lower rates mean lower payments — that part is true. But here's the mechanical problem with that strategy.

When rates drop, affordability improves for everyone at the same time. More buyers enter the market simultaneously, competing for the same inventory. That surge pushes prices up. The lower rate gets partially or fully offset by a higher purchase price. You can get a lower rate, or you can get a lower price. Getting both at the same time is rare — and waiting specifically to capture that combination has cost a lot of Colorado buyers more than it saved them.

Payments get easier — but so does buying for everyone else

More buyers enter the market at once. Demand rises, inventory tightens, and sellers regain leverage. In Colorado's already supply-constrained market, that dynamic moves prices up quickly. Your lower rate may be partially or fully offset by a higher purchase price.

You've paid rent, missed equity, and the math got harder

Every month of rent is a payment with no return. Colorado prices have continued building. Your down payment savings may not have kept pace with appreciation. You're now buying at a higher price with the same rate you could have had a year ago.

What Is Waiting Actually Costing You?

Adjust the inputs to match your situation. The calculator compares where a renter and a homeowner stand at year 3, year 5, and year 10 — in real wealth terms.

How We Got There

See Your Actual Numbers

This calculator uses general assumptions to illustrate the concept. Your real equity picture — built around your actual income, loan terms, tax situation, down payment, and Colorado market — looks different. That's what our MM365 equity builder is for. It takes about 15 minutes with a loan officer and gives you a projection you can actually plan around.

Walk Through the Numbers With UsWhat This Looks Like for a Real Colorado Buyer

David — Colorado

David came to us with his down payment ready and a pre-approval in hand. He kept pushing his timeline back waiting for rates to improve. He was paying $2,200/month in rent and watching the market carefully.

Over the next eight months, rates moved sideways. The home he had originally targeted — listed at $560,000 — sold to another buyer. A comparable home came on the market several months later at $578,000. His rent over those eight months totaled $17,600 — money that built no equity and didn't reduce his future mortgage balance.

When we ran the numbers together, the wait had cost him roughly $35,000 — between the higher purchase price and the rent paid while waiting — for a rate nearly identical to what he could have had eight months earlier. He bought. He doesn't regret it. But he's candid that the waiting felt like a strategy and worked out like a cost.

When Waiting Actually Makes Sense in Colorado

If your credit needs work, your down payment isn't there, or your debt load is too high for favorable terms — waiting to fix those things first is the right call. We map this out clearly in our first planning conversation so you know exactly what you're working toward.

A job change, a possible relocation, a major life transition — these are legitimate reasons to hold off. A mortgage is a long-term commitment, and buying when your situation is unstable creates real risk.

If you're waiting because you don't know what you'd qualify for or what your payment would look like — that's not really waiting, that's uncertainty. A mortgage consult doesn't commit you to anything. It replaces uncertainty with a clear picture of where you stand.

You can explore Colorado loan options on our home loan programs page, including conventional loans and VA loans. Learn more about how we work with buyers on our Colorado mortgage broker page.

The Numbers Mean More With Context

A calculator shows you the math. A real conversation built around your income, savings, and Colorado timeline shows you what it means for you — and whether now, later, or after some prep work makes the most sense. No forms, no pressure, just clarity.

Walk Through the Numbers With UsQuestions We Hear From Colorado Buyers Considering Waiting

They might. But when rates drop, more buyers enter Colorado's market simultaneously — which pushes prices up. The payment savings from a lower rate are often partially or fully offset by a higher purchase price. You can refinance into a lower rate later if rates improve. You can't go back and buy at today's price.

At Colorado's current statewide appreciation rate of approximately 4.2%, the purchase price increases by about $23,000 over 12 months. Add 12 months of rent at $2,000–$2,500/month and the total cost of waiting is typically $47,000–$53,000 in combined price increase and non-equity rent payments. Use the calculator above to model your specific numbers.

Yes. If your credit needs improvement, your down payment isn't ready, your debt load is too high, or your life situation is genuinely uncertain, waiting to address those things first often makes more financial sense than buying before you're ready. A mortgage consult can help you understand whether you're there now or whether a few months of preparation would meaningfully change your options.

MM365 is our proprietary client platform. The equity builder models your ownership position over time — showing what your equity looks like at year 1, year 3, and year 5 based on your actual purchase price, down payment, loan terms, and appreciation assumptions. We walk through it with clients during the planning conversation so the numbers reflect your real situation, not a general estimate.

Florida's market tells a different story right now — prices have softened from their 2024 peak and buyers currently have more negotiating leverage than they've had in years. See our Cost of Waiting in Florida page for market-specific data and analysis.

Cost of Waiting Calculator Colorado Disclaimer

Representative example only. Client details have been generalized to protect privacy. Results are not guaranteed and will vary based on individual financial profiles, lender availability, and market conditions. Bank statement qualification programs are available through select non-QM lenders and are subject to program-specific eligibility requirements. Not all borrowers will qualify. Closing timelines depend on borrower responsiveness, lender processing, and third-party services and may vary.