A Guide to Residual Income Analysis for VA Loans

Residual income represents the funds available after all monthly debts and living expenses have been paid. It’s a critical measure for gauging financial stability, indicating the ability to manage costs while saving or investing. In the context of VA loans, residual income criteria ensure that veterans and military families maintain a healthy financial margin after covering their mortgage and other expenses, promoting long-term financial security.

For veterans, the concept of residual income is especially significant. The VA uses it as a safeguard, ensuring that loan recipients are well-rested by their mortgage payments. This approach reflects a commitment to the financial well-being of service members, emphasizing the importance of having enough income to manage life’s expenses comfortably.

VA Residual Income Guidelines

The VA’s residual income guidelines are designed with the borrower’s financial health in mind. These regulations stipulate minimum residual income levels based on family size and geographic location. The intent is to ensure veterans have sufficient funds after mortgage payments to cover their living expenses, a unique requirement not typically found in conventional loan processes.

The role of residual income extends beyond basic loan eligibility; it is a vital component in the VA loan process aimed at preventing financial distress among veterans. By requiring a certain level of residual income, the VA helps ensure that veterans and their families are better positioned to afford their homes over the long term, reducing the risk of foreclosure and financial hardship.

Understanding the VA’s Residual Income Requirement for Loan Eligibility

The VA implements a residual income requirement to ensure veterans who take out VA loans have sufficient funds to manage their living expenses, including gas, food, clothing, and mortgage payments. This approach is aimed at assessing the affordability of VA loans more accurately, ensuring that homeowners can secure a loan and maintain their lifestyle without financial strain.

The emphasis on residual income is a critical factor in VA loans’ notably low foreclosure rates, even though most VA loan recipients do not make a down payment. By mandating a minimum level of residual income based on the loan size, the borrower’s location, and the household size, the VA aims to safeguard veterans from potential financial difficulties, promoting long-term stability and homeownership sustainability.

Residual Income Calculation

Calculating residual income involves subtracting monthly debts and living expenses from gross monthly income. This figure demonstrates a borrower’s ability to handle additional financial responsibilities, like a mortgage.

For example, if a person earns $5,000 monthly and spends $3,000 on debts and expenses, their residual income is $2,000. This calculation is crucial for VA loans, ensuring borrowers have sufficient funds beyond their immediate obligations.

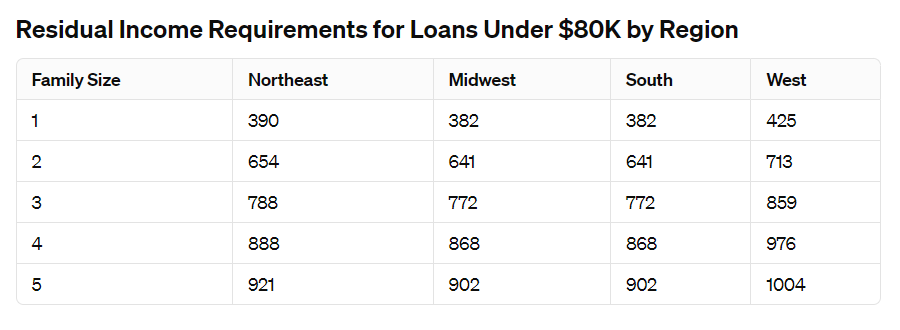

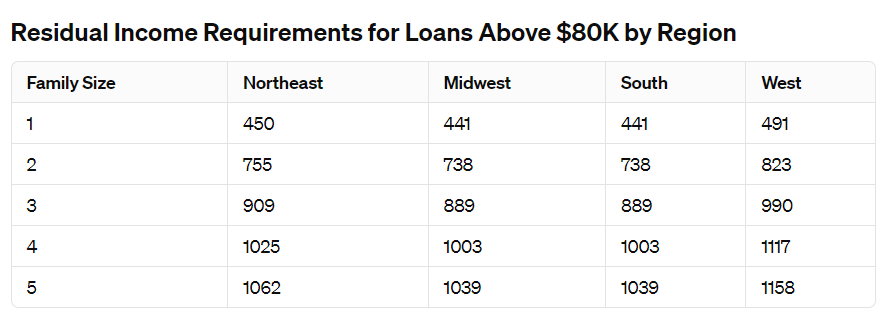

Residual Income Charts

The VA sets minimum residual income requirements that vary by region and family size to ensure veterans can afford their living expenses post-mortgage. For instance, a family of four in the Midwest might need a different residual income compared to a similar family in the Northeast due to varying living costs.

**Add $75 for each additional dependent over 5, up to 7 **

**Add $80 for each additional dependent over 5, up to 7 **

These guidelines are meticulously designed, considering loan amounts and geographic differences, ensuring that veterans nationwide have a fair standard tailored to their specific living conditions.

Impact of Residual Income on Loan Approval

Residual income is pivotal in VA loan approvals, acting as a financial safety net that complements the debt-to-income (DTI) ratio. A solid residual income can significantly enhance a borrower’s profile, especially those with higher DTI ratios.

This is because it demonstrates the ability to manage and sustain financial obligations beyond immediate debts, providing lenders with confidence in the borrower’s economic resilience.

Offsetting Residual Income

Adopting strategic financial planning is key for VA loan applicants seeking to meet or exceed the residual income guidelines. This may include diversifying income sources or reducing monthly liabilities to improve the residual income figure.

Interestingly, certain non-traditional income streams that aren’t directly considered in the loan qualification process could still positively impact the overall financial picture, making it easier to meet VA’s residual income criteria.

The Significance of Residual Income for Veterans

The VA prioritizes residual income because it reflects a veteran’s true financial health beyond traditional metrics like income and credit score. This emphasis helps ensure veterans can comfortably manage their expenses alongside their mortgage, reducing the risk of financial distress.

The adherence to residual income guidelines correlates with lower foreclosure rates among VA loans, demonstrating the effectiveness of this approach in promoting financial stability for veterans.

Conclusion

Residual income analysis is a cornerstone of the VA loan approval process, underscoring the importance of financial preparedness. Veterans and service members are encouraged to understand and meet these guidelines, enhancing their loan eligibility and securing their financial future. This commitment to residual income underscores the VA’s dedication to the long-term well-being of veterans, ensuring they achieve homeownership with a sustainable financial foundation.