Cost of Waiting to Buy a Home in Florida

Florida's housing market has shifted meaningfully over the past year. Prices are below their 2024 peak, inventory is up, and buyers currently have more negotiating leverage than they've had since before 2020. For Florida buyers, the cost of waiting isn't primarily about appreciation pressure — it's about a window of favorable conditions that is tied directly to where rates are right now, and what happens when they move.

This page provides an honest look at where Florida prices actually stand and why today’s "higher-rate" environment may actually be more favorable for your long-term wealth than the high-competition market that follows a rate drop. Use the calculator below to replace the uncertainty of waiting with a clear comparison of your options.

What the Florida Market Is Actually Doing Right Now

Florida is genuinely a buyer's market right now. Prices are down modestly from their peak, sellers are more motivated, and inventory gives buyers real options. The question isn't whether the market is buyer-friendly today — it is. The question is whether those conditions will still be there in 6, 12, or 18 months.

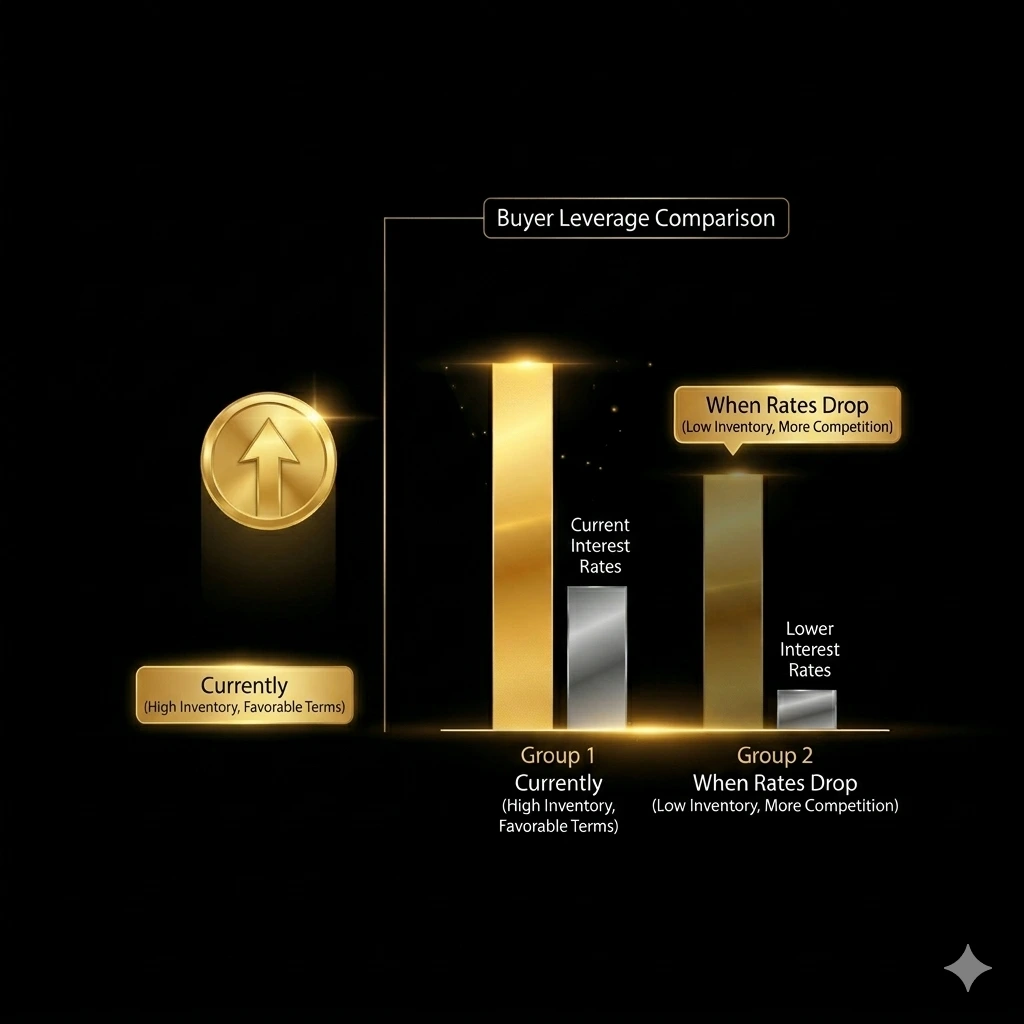

Why the Current Window May Not Stay Open

The rate-price connection in Florida

Florida's current buyer-friendly conditions are directly tied to elevated mortgage rates. High rates have kept buyers on the sidelines, reduced competition, and given inventory time to build. That's exactly what created the negotiating leverage buyers have right now.

When rates drop — and most forecasters expect at least modest decreases in 2026 — that dynamic reverses. Buyers come off the sidelines simultaneously. Demand rises faster than inventory can absorb it. Sellers regain leverage. The motivated sellers and below-peak prices that exist today become harder to find.

Florida Realtors data already showed sales volume picking up in late 2025 as rates ticked slightly lower. The signal is already in the data. The question is how fast it accelerates.

The Trade-Off: Rates vs. Prices in Florida

Your payment gets easier — and so does buying for everyone else

More buyers enter the Florida market simultaneously. The inventory that exists today gets absorbed faster. Motivated sellers become less motivated. The below-peak prices and negotiating leverage that exist right now narrow considerably.

The favorable window closes while you've been paying rent

Every month of rent builds no equity and doesn't reduce your future mortgage. The current buyer's market conditions in Florida — more inventory, motivated sellers, prices below peak — are a specific moment, not a permanent state.

What Is Waiting Actually Costing You?

Adjust the inputs to match your situation. The calculator compares where a renter and a homeowner stand at year 3, year 5, and year 10 — in real wealth terms. Florida's near-term market is flat to slightly negative — adjust the appreciation slider to reflect what you expect.

What This Looks Like for a Real Florida Buyer

Michelle — Florida

Michelle had been watching the Florida market for about a year, waiting for prices to fall further from their 2024 peak. She was paying $2,100/month in rent and felt like patience was being rewarded — prices had softened and there were more homes to choose from than she'd seen in years.

When she came to us for a consult, we walked through the numbers together. Her rent over the 14 months she'd been waiting totaled $29,400. Prices in her target area had dropped about 3% from peak — a savings of roughly $16,500 on a $550,000 home. Net result: waiting had cost her about $13,000 more than buying at the peak, before accounting for the equity she hadn't started building.

More importantly, rates had begun ticking lower and sales activity in her target market was visibly picking up. The negotiating conditions she'd been waiting to take advantage of were starting to thin out. She bought within 30 days of that conversation and got a seller concession of $8,000 toward closing costs — a condition she likely couldn't have negotiated six months later.

When Waiting Actually Makes Sense in Florida

If your credit needs work, your down payment isn't there, or your debt load is too high for favorable terms — waiting to fix those things first is the right move. Buying before you're financially ready tends to cost more than a calculated wait to get there, even in a favorable market.

Florida attracts a lot of buyers in transition — relocations, career changes, retirement moves. If your situation is still in flux, that uncertainty is worth resolving before committing to a mortgage.

If you're waiting because you're unsure what you'd qualify for or what your payment would look like — that's uncertainty, not strategy. A mortgage consult answers those questions without committing you to anything.

You can explore Florida loan options on our home loan programs page, including conventional loans and FHA loans. Learn more about how we work with buyers on our Florida mortgage broker page.

The Numbers Mean More With Context

A calculator shows you the math. A real conversation built around your income, savings, and timeline shows you what it means for you.

No forms, no pressure, just clarity.

FAQs Cost of Waiting Calculator Florida

Florida's market has cooled meaningfully from its 2024 peak and buyers currently have more negotiating power than they've had in years. But that window is tied to current rate levels. When rates drop, buyers come off the sidelines simultaneously — tightening inventory, reducing seller motivation, and putting upward pressure on prices. Waiting for prices to fall further assumes those two favorable conditions stay in place together. They usually don't for long.

Even if Florida prices drop 2% over the next year, the rent you'd pay while waiting largely offsets that savings. At $2,200/month in rent, 12 months of waiting costs $26,400 in non-equity payments. A 2% price drop on a $550,000 home saves $11,000. Net cost of waiting: roughly $15,400, before accounting for equity not built. Use the calculator above to model your specific numbers.

Lower rates actually close the current buyer-friendly window in Florida fastest. They bring more buyers into the market at the same time, tighten available inventory, and reduce the negotiating leverage that buyers currently have. The below-peak prices and seller concessions that exist today are a function of elevated rates keeping buyers on the sidelines. When that changes, the conditions change with it.

Yes. If your credit needs improvement, your down payment isn't ready, your debt load is too high, or your situation is in transition — waiting to address those things first often makes more sense than buying before you're ready. Florida also attracts a lot of relocation buyers, and if your move isn't finalized yet, resolving that first is the right call.

Colorado's market tells a different story — prices are continuing to appreciate modestly and the cost-of-waiting argument is more directly about rising purchase prices. See our Cost of Waiting in Colorado page for market-specific data and analysis.

Cost of Waiting Calculator Florida Disclaimer

Representative example only. Client details have been generalized to protect privacy. Results are not guaranteed and will vary based on individual financial profiles, lender availability, and market conditions. Bank statement qualification programs are available through select non-QM lenders and are subject to program-specific eligibility requirements. Not all borrowers will qualify. Closing timelines depend on borrower responsiveness, lender processing, and third-party services and may vary.