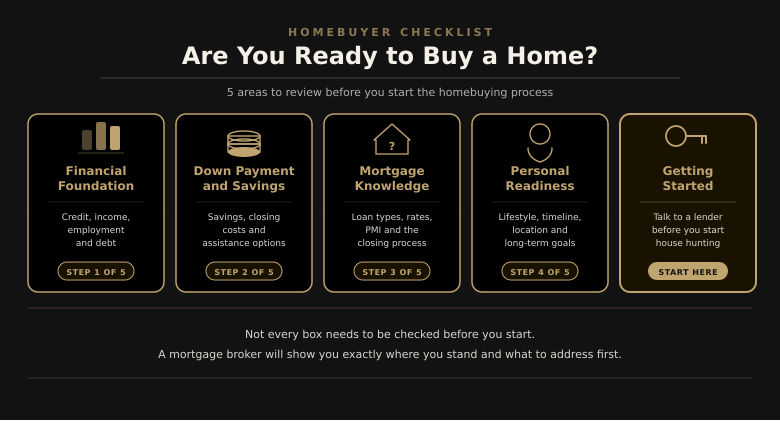

Home Buying Readiness Checklist

A home buying readiness checklist is the most useful thing you can work through before starting the mortgage process. It tells you exactly where you’re strong and where you have gaps.

This one covers five areas: credit, savings, income stability, mortgage knowledge, and personal readiness.

Work through each section honestly. You don’t need to check every box to move forward, but knowing where you have gaps helps you plan smarter and avoid surprises.

Most buyers find that going through a home buying readiness checklist like this one surfaces one or two things worth addressing before they apply.

Before We Start

Two quick questions calibrate your results, some items on this checklist don’t apply to every loan program.

Financial Foundation

These are the building blocks lenders look at when assessing your financial readiness for homeownership. Knowing where you stand here tells you a lot about how prepared you are.

Down Payment and Savings

Your down payment gets the most attention, but it’s not the only cash you’ll need at closing. This section covers the full picture.

Mortgage Knowledge

You don’t need to become an expert, but understanding the basics helps you ask better questions and recognize a good deal from a bad one.

Personal Readiness for Homeownership

The financial side matters, but so does your life situation. These questions help you think beyond the numbers, and they’re part of any honest home buying readiness assessment.

Getting Started: Your Home Buying Readiness Action Plan

These are the practical steps that move you from “thinking about it” to “doing it.” Working through this home buying readiness checklist is a meaningful step forward, and even one or two checked boxes here means you’re making real progress.

Where Does Your Home Buying Readiness Stand?

Your financial foundation is where to focus first.

The items in the first two sections, your credit picture, income stability, and path to a down payment, have the most direct impact on what you qualify for and at what rate. Knowing loan types or having a real estate agent in mind matters less right now than getting those fundamentals clear.

- Pull your free credit reports at AnnualCreditReport.com, your score determines which loan programs are available to you and heavily influences your rate

- Calculate your debt-to-income ratio: add up monthly debt payments and divide by gross monthly income, most loan programs cap this at 43–45%

- Explore Colorado down payment assistance programs, eligibility often surprises people

You have real momentum, a few gaps are worth closing before you apply.

Your financial basics are taking shape, but there are likely items in your savings picture or knowledge of the process that could affect your loan options or create friction during underwriting. Addressing them now costs nothing and puts you in a significantly stronger position when you apply.

- Get your full cash picture in order: down payment, closing costs (typically 2–5% of the loan amount), and a post-closing buffer, lenders verify all three

- Start gathering your financial documents, two years of tax returns, recent pay stubs, and 2–3 months of bank statements speed up pre-approval significantly

- Have a conversation with a mortgage broker before you think you’re ready, a 20-minute call clarifies your actual buying power and what specifically to address next

Your financial position is strong, pre-approval is the logical next step.

You’ve addressed the things that actually determine mortgage eligibility: your credit, income stability, and your path to a down payment. The buyers who get to closing smoothly are the ones who did this work before they started shopping. Pre-approval gives you a real number, signals serious intent to sellers, and typically takes less time than people expect.

- Connect with a Colorado mortgage broker to start the pre-approval process

- Compare programs, conventional, FHA, and VA loans each have different trade-offs based on your down payment amount and credit profile

- Begin your home search with a pre-approval letter in hand, it changes how agents and sellers respond to your offers

Helpful Resources to Support Your Homebuying Readiness

Important Disclosures

Elevation Mortgage LLC | NMLS# 2179191 NMLS Consumer Access

This checklist is provided for educational and informational purposes only and does not constitute a loan commitment, loan approval, or offer to extend credit. All loan programs, down payment requirements, and eligibility criteria referenced are general in nature and subject to change without notice. Actual qualification requirements vary by loan program, lender, borrower profile, property type, and prevailing market conditions.

References to down payment percentages, including figures such as 3% down or less than 20% down, are illustrative general examples only and do not represent specific loan offers, advertised credit terms, or commitments to lend. These figures are included solely to help readers understand general program categories and planning considerations. Loan approval is subject to full credit review, income and asset verification, property appraisal, and all applicable underwriting requirements. Not all applicants will qualify for all programs.

Any reference to pre-approval on this page is based on a preliminary review of information provided at the time of inquiry. Pre-approval does not guarantee final loan approval. Final approval is contingent upon satisfactory verification of all submitted information, receipt of an acceptable appraisal, and fulfillment of all remaining loan conditions prior to closing.

Licensed in Colorado. Colorado: Regulated by the Colorado Division of Real Estate.

Ⓡ Equal Housing Opportunity. Elevation Mortgage LLC does not discriminate on the basis of race, color, religion, national origin, sex, disability, or familial status in the terms, conditions, or privileges of residential mortgage lending.