Stop Guessing, Start Moving

We show you everything...

Before you ask.

In the high-stakes world of real estate, most mortgage companies are still using outdated maps.

The standard practice is to guess early, capture the sale, and hope the underwriter doesn't find a problem later. This "hope-and-pray" strategy backfires on Day 15, right before closing, when the bank’s hidden internal guidelines finally clash with your reality. The result is a late denial, leaving you with packed boxes and zero recourse.

That is not the Elevation Mortgage way.

We act as your financial guardian. We do not "sell" loans; we engineer bulletproof mortgage plans. We deploy a proactive underwriter-verification process on Day 1, ensuring the internal math is sound before you gamble your savings.

This is the strategic code we use to protect you:

1. Hard Math is Our Strength: If you own a business or have a complicated job, big banks treat you like a problem. We treat you like a pro. We use a special Safety Check to prove your income so the underwriter understands how hard you work.

2. A Fast "No" is Better Than a Late "Maybe": We do not guess. We check every page of your taxes and paystubs before you go house hunting. If the math does not work, we tell you on Day 1. If it does work, you can shop knowing your money is safe.

3. We Are a Team: Getting your keys in 21 days is a team sport. Our job is to give you a clear map. Your job is to be a fast partner and send paperwork quickly.

4. We Protect Your Savings: In a tough market, your deposit money is at risk. We act as your Shield. If a deal is not "bulletproof," we will not let you sign it.

5. No More Secrets: Most lenders keep you in the dark. We pull back the curtain. You deserve to know exactly what the underwriter is looking at.

Ready to kill the chaos?

BOOK YOUR CALL WITH RYANIf you are just starting to buy a home, it is normal to feel like you are missing a map.

Most guides are too vague and skip the parts that actually matter.

The truth is simple: Most lenders guess and hope.

They say "Yes" on Day 1 just to make a sale, but say "No" on Day 15 after an underwriter looks at your file.

This leaves families with packed boxes and lost money.

According to the CFPB's homebuying resource center, most buyers wish they had a better map before they started.

At Elevation Mortgage, we do more than just show you the map and where the process can break down.

We review your entire file on Day 1 so nothing gets missed.

We do this work early so you do not lose your deposit on Day 15.

This page shows the real process we use with our clients, step by step.

Jump to your current stage

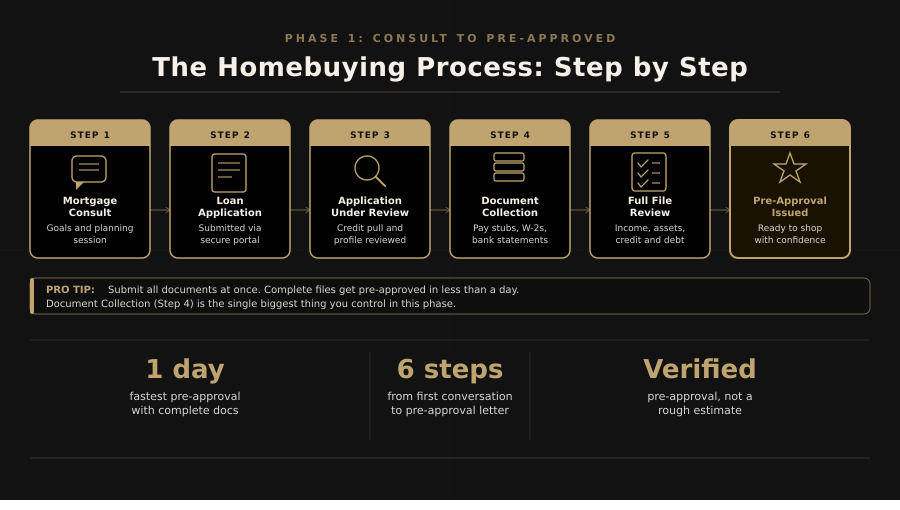

Phase 1: Mortgage Strategy Consult to Pre-Approved

Most lenders skip the preparation because it is hard work. They jump straight to an application, which usually backfires. The "Hard Math" we do in Phase 1 directly shapes your rate and ensures Phase 2 is a sprint, not a struggle.

Stage: Mortage Strategy Call

What happens: We will sit down for 30 minutes to look at the "big picture" of your life and money. This is more than just a quick chat. We are going to look under the hood of your finances to see how you earn your money, what you’ve saved, and exactly what kind of monthly payment makes sense for your lifestyle. We will also talk about your "Must-Haves" for your new home.

Why it matters: Most lenders just look at a credit score and say "Go." We do the opposite. We look for "money traps" now. Hidden debts or complicated tax paperwork could jump out and scare an underwriter later. By doing a deep dive on Day 1, we make sure that when you find the perfect house, the bank says "Yes" without a fight.

What we cover on this call:

- Your Real Budget Not just what the underwriter allows, but what you are comfortable paying every month.

- Income Secrets If you are self-employed or have a unique job, we figure out exactly how to show that to the underwriter so they understand your income.

- The Game Plan We talk about where you want to live and how much of your own money you want to keep in your pocket versus putting into the house.

Stage: Application Sent

What happens: We will send a secure link to your email. You will spend about 15 minutes typing in the basics: who you are, where you’ve lived, where you work, and what you own. This is a simple digital form, but it’s the most important piece of paper in the whole process.

Why it matters: This isn’t just "info". This is your official story. We use this data to decide if you are a "safe" person to lend money to. If there are small mistakes here, it can cause big delays later. By doing this right the first time, we make sure the bank sees you as a professional.

The "Insider Secret" to a Strong File

- List Every Account A common mistake is leaving out bank accounts you aren't using for the down payment. Don't do this. Even if you aren't spending that money, the bank wants to see it. It shows them you have "backup cash" for emergencies, which makes your file much stronger and easier to approve.

- The Basics Your full legal name, your last two years of home addresses, and your current job info.

- Total Honesty This is where you tell the truth about everything. If we find a "surprise" later that isn't on this form, it can kill the deal.

Stage: Application Received

What happens: Once you hit "Submit," my team jumps in. We don't just put your file in a pile; we open it up and check every line. We make sure your info matches the underwriting guidelines and we look for red flags so we can address them now, not later.

Why it matters: In the mortgage world, small mistakes become giant headaches later. If the underwriter finds a mistake on Day 15, it could stop you from getting your keys. We "scrub" your application now so that by the time the underwriter reviews your file, it’s perfect. This saves you time and keeps your stress low.

What we are looking for here:

- The Math: We double-check that your income and your debts match up.

- The "Local" Rules: Colorado and Florida have different taxes and insurance rules. We make sure your file follows the right ones.

- The Clear Path: If we see anything that might confuse the underwriter, we fix it before moving to the next step.

Stage: Waiting on Documents

What happens: This is where you hand over the "Big Five" proof: your W2s, Tax Returns, Paystubs, Bank Statements, and your ID. You’ll upload these to our secure portal. We need every single page of every document—even the ones that are blank or just have small print.

The 24-Hour Goal: We ask that you get these to us within one day. We can’t review your file until we have the supporting documents to back it up. Think of it like a race: we are standing at the starting line, but we can't run until you give us the baton.

Why it matters: Most people wait until they find a house to get their paperwork ready. That is a huge mistake. If we find a "money trap" in your taxes on Day 1, we have time to fix it. If we find it after you sign a contract, you could lose your deposit money. We move fast now so you can shop with a "Shield" around your money.

What to remember here:

- Every Page Counts: If a bank statement says "Page 1 of 6," the bank will demand all 6 pages. If one is missing, they won't even look at your file.

- No Screenshots: We need the real PDF files or clear scans. We can’t read a blurry photo from a phone.

- The "Full Picture": Remember Step 2? Send us the statements for every account you own, even the ones you aren't using for the house. It makes your file look much stronger to the underwriter.

Stage: Loan Review

What happens: This is where we go to work. We don’t just "look" at your papers; we put them through a high-tech "Safety Check." We use special software built with all the underwriting guidelines to read your taxes and check your bank accounts. Then, we personally review the output to make sure it didn't miss a single detail. We put a "human eye" on your file to make sure it's perfect. No AI hallucinations!

Why it matters: Most lenders just "guess" and hope for the best. We do the hard work now so there are zero surprises later. By running your info through our system before you even find a house, we find any "money traps" that could stop you from getting your keys. This is how we "guarantee" your loan will close on time.

What we are doing for you here:

- The Math Check: We make sure every dollar of your income is counted the right way so the underwriter understands your strength.

- The Rule Check: Loan guidelines have thousands of rules. Our software knows them all, so we can be sure your file passes the test.

- The Human Touch: A computer is fast, but a human is smart. We look at your file like a partner to make sure you have the strongest case possible.

Stage: Pre-Approved

The Result: You get your Official Pre-Approval Letter. This isn't just a piece of paper; it’s a "Verified Guarantee" from my team that your math is solid. It tells any seller that you are ready, willing, and able to buy their house right now.

Why it matters: In today’s market, houses sell fast. When you find a home you love, you don't want to wait. This letter gives you "Buying Power." When a seller sees our letter, they know we’ve already done the hard work. They know they can trust your offer, which helps you win the house even if other people are bidding on it.

What this letter does for you:

- Total Confidence: You can walk into any house knowing exactly what it will cost you and that the underwriter is already on your side.

- Winning Power: Sellers in Colorado and Florida love our letters because they know we don't make mistakes. Your offer goes to the top of the pile. Plus, we call every listing agent to explain our process and how we ensure a smooth closing.

- Fast Action: The moment you find "The One," we are ready to move. No waiting, no guessing, no stress.

Stop Guessing.

Start Your Ironclad Pre-Approval.

Get your verified game plan so you can shop without the chaos.

START YOUR MORTGAGE STRATEGY CONSULTDirect Client Reviews

Real stories from the closing table

Reed was an outstanding professional to work with! He helped us understand which mortgage option was best for us and was always very responsive to questions. I highly recommend him and his company if you are looking for a mortgage company.

"Reed has always been one of the best mortgage brokers to work with. He has the best rates and has always gotten the deal to the closing table."

"Reed is great to work with. He is professional, caring and very responsive in helping you out with your mortgage."

"Elevation Mortgage has been rock solid with assisting buyers that I've sent their way. As a Realtor I have high expectations for my lender partners and Elevation is outstanding. Very professional, knowledgeable, responsive and thorough! Do not hesitate to reach out to the top mortgage broker in Colorado Springs, you'll be glad you did."

"DO NOT limit yourself by working with a retail mortgage lender who can only offer you limited products. Reed and his team are knowledgeable and professional. Getting approved for a mortgage is not out of reach with the knowledge, resources and experience this team brings to the table. Highly recommend this company for new loans, refinance or just getting prepared for becoming a new home owner in the future. Elevation Mortgage has earned our lifetime business!"

"I represented Buyers who got their mortgage from the Letson Group and Reed and his team were responsive, professional, and quick to problem solve as we had some last minute hoops to jump through on the Real Estate sale. They offer more diverse loan options than a standard bank and their rates are competitive. I recommend them!"

"My wife and I recently purchased a home with the assistance of two highly qualified, technically competent, and hard-working gentlemen. Ryan Nash is one of those gentlemen. Ryan was always connected and quick to answer any questions we had. He would dig in and find the answer if he didn’t know the answer. He intuitively knew what follow-up questions we would have and had the answer ready or provided. I cannot say enough good things about the services, effort, and attention to detail Ryan provided. He IS the proverbial easy button!"

"Ryan was absolutely fantastic. I had a very challenging situation, attempting to buy a new home prior to selling our existing one. He somehow made the impossible possible and we closed on the new home! Professional, knowledgeable, extremely responsive, and just overall an amazing person to work with. He found creative solutions for my unique situation and went above and beyond to make the process as smooth as possible. I can confidently say that without his help, we would not be currently moving into our new home. I can't thank you enough, Ryan!"

Not Ready Yet?

We Don't Walk Away.

Most lenders say "No" and disappear. We stay with you and build a plan to get you to "Yes."

The Honest Assessment

Sometimes the math just doesn't work today. Maybe your credit score is a little too low, or you need a few more months of income history. We tell you exactly where you stand — on Day 1, not Day 15.

Your Written Roadmap

We build you a step-by-step plan that tells you exactly what to do to get your "Yes." Which bills to pay, how much more to save, how to fix a mistake on your credit report. We do the thinking so you just follow the steps.

We Fix the Math Together

Credit scores, debt ratios, income gaps — we show you exactly which numbers to move and by how much. No guessing, no generic advice. Just the specific steps that get your file approved.

We Stay With You

We check in with you along the way. When you hit the milestones on your roadmap, we run the numbers again. Most clients on a "Not Yet" plan are ready to go back to Step 6 within 60 to 90 days.

Not sure where you stand? Let's find out together — no pressure, no forms, just an honest look at your situation.

GET YOUR FREE ROADMAPPhase 2: Under Contract to Closing Day

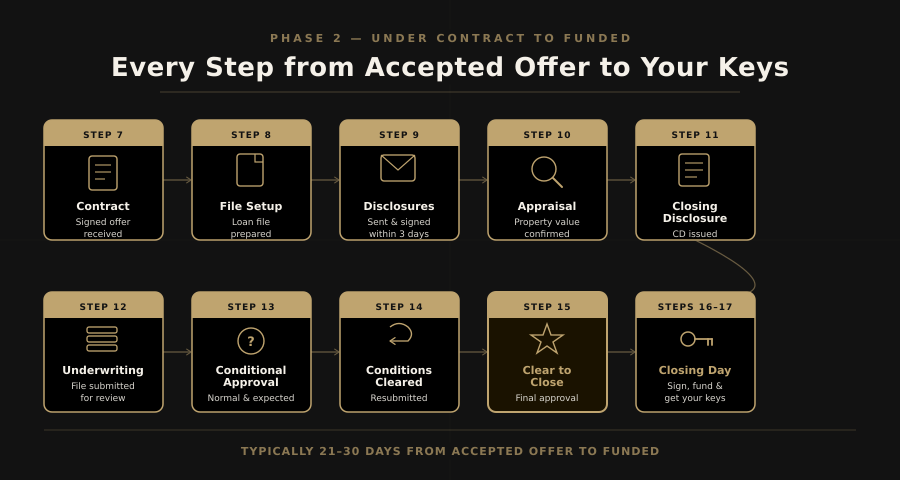

Once a seller accepts your offer, the second phase of the homebuying process begins — and the clock starts. This phase typically runs 21 to 30 days. A lot happens in that window, and most of it runs in parallel. Here's every stage in the order it happens.

Stage: Contract Received

What happens: The moment the seller signs your offer, we need a copy. This officially starts the race. We also double-check your paperwork. If it’s been a few weeks since Step 1, we might need a fresh paystub or bank statement to keep your file current.

Why it matters: The bank wants to see exactly what is happening right now. Keeping your documents fresh ensures the bank doesn't hit the "pause" button later.

⚡ The Speed Trigger:

Stage: Loan Setup

What happens: We build your "Official File" using the house address, the purchase price, and the closing date.

Why it matters: Everything from here on out must be 100% accurate. We build a solid foundation now so the rest of the house doesn't shake.

⚡ The Speed Trigger:

Stage: Disclosure Package

What happens: We send you a big digital stack of papers to sign. These papers show the "Estimated" costs and rules of your loan.

The Truth: Signing these doesn't mean you are "locked in" or forced to take the loan. It just means, "I received this info and I’m ready to move forward." We can't move to Step 10 until these are signed!

⚡ The Speed Trigger:

Stage: Appraisal & Inspection

What happens: This is where we prove the house is worth the money and that it is safe to live in. We hire a professional (the Appraiser) to visit the home and give us a final value. But before that happens, you will have your own Home Inspection to find any broken items or needed repairs.

Why it matters: The bank will not lend money on a house that is broken or overpriced. We have to coordinate the timing of the inspection and the appraisal perfectly to keep your 21-day clock moving.

⚡ SPEED TRIGGERS

- Pay for the Appraisal Immediately: The Appraiser will not even put you on their calendar until they are paid. As soon as we send you the payment link, pay it. Every hour you wait is an hour added to your closing date.

- The Inspection Resolution: Once your home inspector finds issues, you and the seller will sign an agreement on what needs to be fixed. Send us this signed paper the second it is finished. We cannot move to the next step without it.

- The "Repairs First" Rule: If the seller agrees to fix things, the Appraiser cannot go to the house yet. We must wait until every single repair is 100% finished. If the Appraiser goes out and the work isn't done, the bank will charge you for a second visit and your closing will be delayed.

- The Contractor Race: If the house needs repairs, you must ask the seller: "How fast can your contractor get this done?" You need a team that can finish in 48 hours. If repairs take a week, you will not close in 21 days.

⚠️ TRUTH-TELLER TIP: We want the Appraiser to see a perfect house the first time. If we send them out while the kitchen is still torn apart or the roof is being fixed, the underwriter will hit the "Emergency Brake" on your loan. Fix first, appraise second.

Stage: Closing Disclosure

What happens: This is a 3-part process to show you the final math. Once we have the "final numbers" from the title company, we issue the disclosure in three stages:

- Initial CD: This is the "First Draft." We send this to you to review the numbers and make sure everything looks correct based on our earlier strategy calls.

- Signed CD: Once you sign this, a mandatory 3-day federal "Cooling Off" clock starts. By law, you must have these 3 days to review the math before you are allowed to sign your final loan papers.

- Final CD: This is the "to-the-penny" version. After the 3-day clock runs out, we issue this final version which matches the wire transfer you'll send to the title company.

Why it matters: The Closing Disclosure is the final "ledger" of your home purchase. It summarizes the final loan terms, your monthly payments, and exactly how much you will pay in fees and closing costs. It ensures there are no "surprises" at the closing table.

⚡ The Speed Trigger:

Stage: Submit to Underwriting

What happens: We send your whole file—taxes, insurance, and the house contract—to the bank’s official "Judge" (the Underwriter).

Why it matters: This person makes the final decision. They look at everything with a "human eye" to make sure it follows all the rules.

Stage: Approved with Conditions

What happens: This is a normal part of every loan. The Underwriter usually says, "Yes, but I need 2 or 3 more things."

Why it matters: It’s not a red flag! They might just need a letter explaining a deposit or a fresh bank page. We will tell you exactly what they need and why.

⚡ The Speed Trigger:

Stage: Resubmittal

What happens: Once we get those last items from you, we send them back to the Underwriter.

Why it matters: This is the final "back-and-forth" to make sure the bank is happy. Quick responses here protect your move-in date!

Stage: Clear to Close

What happens: This is the best news! The Underwriter gives the "All Clear." You sign your Final CD at least 3 days before you move.

Why it matters: The hard work is done. The bank is officially ready to send the money.

Stage: Closing Day

What happens: We send the final papers to the Title company. You’ll go to their office to sign your name (a lot!) and do one last walkthrough of the house. Once the ink is dry, the bank sends the money (the Wire) and the county records the deed.

The Timing: Signing usually takes about 45–60 minutes. Once the wire hits, you officially own the home!

The Finish Line: This is the moment you get your keys. Congratulations! You’ve successfully navigated the 21-day race and reached your goal.

Ready to start your 21-day sprint?

The clock moves fast once you're under contract. Get the team that knows how to win the race without the last-minute stress.

BOOK YOUR STRATEGY CALL700+ CLOSINGS. ZERO CHAOS.

Phase 3: The Guardian (Post-Close & Beyond)

The Mission: Most lenders stop working the moment your loan is funded. We don't. Our goal is to ensure your home remains your most powerful wealth-building tool, long after you get the keys. We actively monitor your loan so your mortgage stays aligned with your life, your budget, and your long-term financial freedom.

Here are 4 things we do after closing:

Stage: The Annual mortgage Review

What happens:Once a year, we sit down for 15 minutes to look at your "Home Wealth." We check how much your home is worth now and how much you still owe the bank. We also do a deep dive into your Real Estate Taxes and your Home Insurance.

Why it matters:Your life changes, and so do the costs of owning a home! Taxes and insurance can change dramatically. We look for ways to save you money that have nothing to do with interest rates. We check if you are overpaying for insurance or seeing if you can stop paying for "Mortgage Insurance" (PMI). Whether you want to renovate the kitchen or pay off a high-interest credit card, we make sure your monthly payment is inline with your budget. .

Stage: Equity Growth

What happens:We keep a close eye on what your home is worth compared to what you owe. That extra value is called Equity.

Why it matters: You don't have to leave that money sitting "inside the walls" of your house. We show you how to wake up that "sleeping money" and put it to work. You can use your equity to invest in the stock market, buy an investment property, or pay off high-interest debt. We help you move money from your house into things that actually grow your net worth and build long-term wealth.

Stage: Wealth Strategy

What happens: We watch the math for you so you don’t have to guess. We look for a "Break-Even Point"—this is the exact moment when changing your loan saves you more money than it costs to do the paperwork.

Why it matters: We aren’t "rate shopping" just to stay busy. We only suggest a move if the math is bulletproof and puts more cash in your pocket every single month. We watch the market every day so you can focus on your life, knowing that if there is a way to save money, we will be the first ones to tell you.

Stage: Financial Partner For Life

What happens: Most lenders disappear the moment they get paid. We don’t. We stay by your side for every "What If" question that comes up as your life grows. We provide the math and the options so you can make the best choices for your family’s future.

Why it matters: We want your home to be a tool for your freedom, not a burden. We help you compare your options:

- The Stock Market We can show you how to take extra cash or home equity and invest it in the market to grow your long-term wealth.

- Early Payoff If you prefer the safety of a debt-free home, we show you the "Small Move, Big Win" math. We'll show you how adding a little extra to your payment can shave 5 or 10 years off your mortgage.

Build Wealth. Not Just Debt.

Most lenders see a transaction. We see your most powerful financial tool. Get the strategy that protects your home and grows your net worth for life.

SECURE YOUR FINANCIAL GUARDIAN700+ CLOSINGS. ZERO CHAOS.

FAQs Homebuying Process

Phase 1 — from your first consult to pre-approval — can take anywhere from one day to several weeks depending on how quickly documents come in and whether any prep work makes sense first. Phase 2 — from accepted offer to funded — typically runs 21 to 30 days. A realistic total timeline for a well-prepared buyer is 60 to 90 days from first conversation to keys, though it varies based on your situation and the market.

Before — and the earlier the better. Talking to a lender first tells you what you can actually afford, surfaces anything worth addressing before you apply, and puts you in a position to move quickly when you find the right home. Buyers who skip this step often lose out on homes because they can't get pre-approved fast enough, or they fall in love with a home that doesn't fit their actual financial picture.

It means the underwriter has reviewed your file and is prepared to approve the loan once specific items are resolved. This happens on nearly every loan — it's a normal part of the homebuying process, not a warning sign. Conditions range from internal items we're waiting on, like the appraisal or title work, to things we may need from you, like an updated bank statement or a short letter of explanation. We'll always walk you through exactly what's needed and why.

The Loan Estimate is sent early in the process — within three business days of submitting your application with a property address. It shows your estimated loan terms, rate, monthly payment, and closing costs. The Closing Disclosure comes later, once your loan is fully approved, and shows your final actual numbers. By law, you must receive and sign your Closing Disclosure at least 3 business days before closing. If anything changes your loan terms after we issue it, we reissue it and that 3-day window resets.

Yes — they're completely different things. The appraisal is ordered by the lender to determine the market value of the home. It's not a condition report. The home inspection is hired by you to assess the physical condition of the property — roof, foundation, electrical, plumbing, HVAC, and more. The lender doesn't require an inspection, but buying without one means buying without knowing what you're actually getting. In Colorado, a radon test is also worth adding — Colorado has some of the highest radon levels in the country.

The "Black Box" Checklist

Most lenders say "Yes" just to get your business.

Use these 7 questions to see if they have a real system or if they are just guessing with your money.

The Trap: If they say "I’ve been doing this for 20 years" or "Just trust me," run.

The Truth: A professional should have a clear, written structure (like our Roadmap) that shows exactly how they check your math before you go shopping.

The Trap: If they give you a range like "usually 20 to 30 days," they aren't measuring their work.

The Truth: A lender who doesn't know their own numbers can't protect yours. You want a lender who knows their average down to the day.

The Trap: If they just say "The computer handles it" (or mention "AUS"), that isn't enough.

The Truth: Computers miss things. You need to know they have a specific Human + Software Checklist designed to find the "hidden" problems that could kill your deal at the last minute.

The Trap: Most lenders just email a PDF and disappear.

The Truth: In a tough market, your lender should be your "hype man." They should call the seller's agent to explain why your offer is the safest one on the table.

The Trap: If they say "We check your rate," they are just looking for another sale.

The Truth: A real partner reviews your Taxes, Insurance, and Home Equity. They should help you see if you can delete your PMI or use your equity to invest in the stock market.

The Trap: Big banks shuffle you between "departments."

The Truth: You need one person who knows your "financial skeletons" and your goals, so you don't have to explain your life five different times.

The Trap: A salesperson will hang up if the deal is "too hard."

The Truth: A partner stays with you. They should provide a plan that tells you exactly what to fix so you can buy a home later.

Costs Most Buyers Don't Plan For

Down payment gets most of the attention. But there's a category of costs that reliably catches buyers off guard — especially first-timers. Colorado's CHFA program offers down payment assistance for qualified buyers, but these additional costs are typically still the buyer's responsibility. Use our mortgage calculator for payment estimates, then factor in the table below for the full picture.

| Cost | Typical Range | When It's Due | Notes |

|---|---|---|---|

| 🚩 Home Inspection | $350–$600 | Within days of going UC | Your lender doesn't require it — but skipping it is a real risk |

| 🚩 Radon Inspection (CO) | $125–$200 | Same time as inspection | Colorado-specific; first-timers consistently overlook this |

| 🚩 Appraisal | $500–$900 | After disclosures signed | Your lender requires it; we order it; you pay for it |

| 🚩 Closing Costs | 1% – 5% of loan amount | At closing | Includes lender fees, title, recording, prepaid items |

| ✅ Homeowners Insurance | $2,000–$4,000/yr | Before or at closing | You typically pay the first year upfront; must be in place before funding |

| ✅ Moving Costs | $500–$3,000+ | Around closing | Easy to underestimate — plan for this early |

What A 21-Day Win Looks Like

Most buyers wait until they find a house to get serious. Jamie and Chris did the opposite, which is why they hit their 21-day goal without breaking a sweat.

- The Pre-Game: Before even looking at houses, they submitted 100% of their documents. We identified a credit balance and a tax question, clearing those hurdles before the pre-approval.

- The Sprint (Day 1): The moment they went Under Contract, they didn't wait to be asked, they immediately uploaded fresh, current paystubs and bank statements to replace the older ones from their pre-approval.

- The Pivot (Day 5): When the Home Inspection turned up a Radon issue, they negotiated the fix and sent us the signed resolution the same hour.

- The Finish (Day 14): Because the file was so "clean" from the start, the Underwriter gave the Clear to Close a full week early.

The Result: They signed their Final CD on Day 18 and closing took place on Day 21. No stress, no "Emergency Brake," just a moving truck on schedule.

Curious Where You Actually Stand?

The roadmap shows you every stage. A real conversation shows you which stage you're starting from and exactly what prep work is worth doing before you apply. No pressure, no forms, just an honest look at your situation.

Homebuying Process Disclaimers

This page is provided for educational purposes only and does not constitute an advertisement for a specific loan product or an offer or commitment to lend. Loan approval is subject to credit review, income verification, appraisal, and satisfaction of all applicable underwriting conditions. Not all borrowers will qualify. Loan programs, rates, terms, and availability are subject to change without notice. Pre-approval is based on a preliminary review of credit information only and is not a commitment to lend. Final loan approval is subject to full underwriting review, property appraisal, title clearance, and satisfaction of all conditions.

Colorado: Regulated by the Division of Real Estate. Florida: Licensed by the Office of Financial Regulation.

Equal Housing Opportunity. Ⓡ